[ad_1]

Listed below are some issues I believe I’m occupied with:

1) 2023, the 12 months of Disinflation?

In my annual outlook I mentioned that 2023 was going to be the yr of disinflation. My guess is that Core PCE ends the yr round 3%. That’s greater than the Fed’s 2% goal nevertheless it’s all transferring in the correct course.

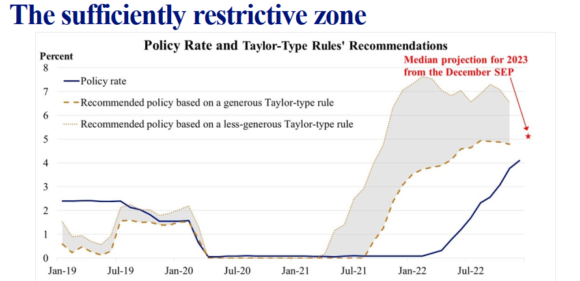

I used to be fairly pleasantly shocked to see that James Bullard from the Fed, has the same view of issues. In a latest presentation he mentioned that 2023 was prone to be a yr of disinflation. And like my outlook, he mentioned {that a} 5% in a single day charge could be sufficiently restrictive. This was the important thing chart from his presentation which exhibits how the coverage charge and Taylor Rule are prone to converge because the yr strikes on.

So, on the one hand I’m glad to see that Fed officers have comparable outlooks to mine. However, ought to I be involved that Fed officers, who have been at 0% only a yr in the past, have the identical outlook? Yikes.

2) The Progress Bubble Hasn’t Popped?

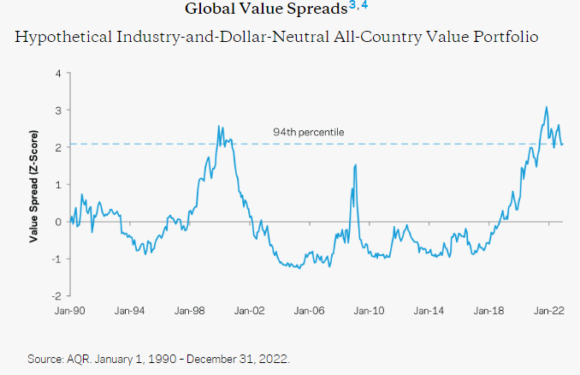

Right here’s a considerably provocative piece from Cliff Asness who says that the bubble in development shares nonetheless hasn’t popped. He doesn’t truly write something, however as an alternative simply posts this chart. The implication being that worth shares are massively undervalued relative to development. Even after development was a catastrophe in 2022. Cliff’s apparent view is that this relative valuation has rather a lot additional to compress.

What’s my view? I don’t know to be trustworthy. I don’t usually love the concept of “issue” investing as a result of it’s in the end simply one other type of inventory choosing the place you’re attempting to select which sectors or segments of the market are “development” vs “worth” (no matter these phrases truly imply). So, as an example, utilizing this chart you’ll have been bearish about development from 2018 on, suffered by way of 3 years of brutal underperformance earlier than lastly being proper in 2022 (whenever you nonetheless misplaced cash). To me all of it strengthens the outdated Bogle argument for “purchase the haystack, ignore the needle” method.

But when we’re wanting on the market as entire then sure, I agree with Cliff that the fairness market as an entire nonetheless appears very dangerous. So that might result in the conclusion that greater danger greater development names are prone to be riskier than decrease beta sort names. Are you able to decide which shares are going to appear like development or worth going ahead although? That’s a a lot messier endeavor in my opinion.

3) Classes From 2023

I liked this interview with Christine Benz from Morningstar. In a single section she discusses bucketing methods and the worth of understanding the period of your bond allocation. She particularly discusses the significance of matching durations with money circulation wants so that you don’t end up ready the place you want one thing to be principal protected that truly finally ends up fluctuating rather a lot.

That is just like the teachings from 2022 that I mentioned late final yr and it’s been the principle impetus for creating my “All Period” technique. However as an alternative of making use of the idea of “period” solely to bonds we’ve utilized it to all asset lessons in order that an investor can construction a portfolio in a really particular planning based mostly method the place they bucket segments in accordance with their precise monetary planning wants. This helps put issues just like the inventory market or long-term bonds within the correct “bucket” so that individuals can particularly perceive how their property match with their future anticipated liabilities.

Go give a take heed to the interview with Christine. She’s probably the greatest round.

Please comply with and like us:

About Put up Creator

[ad_2]