[ad_1]

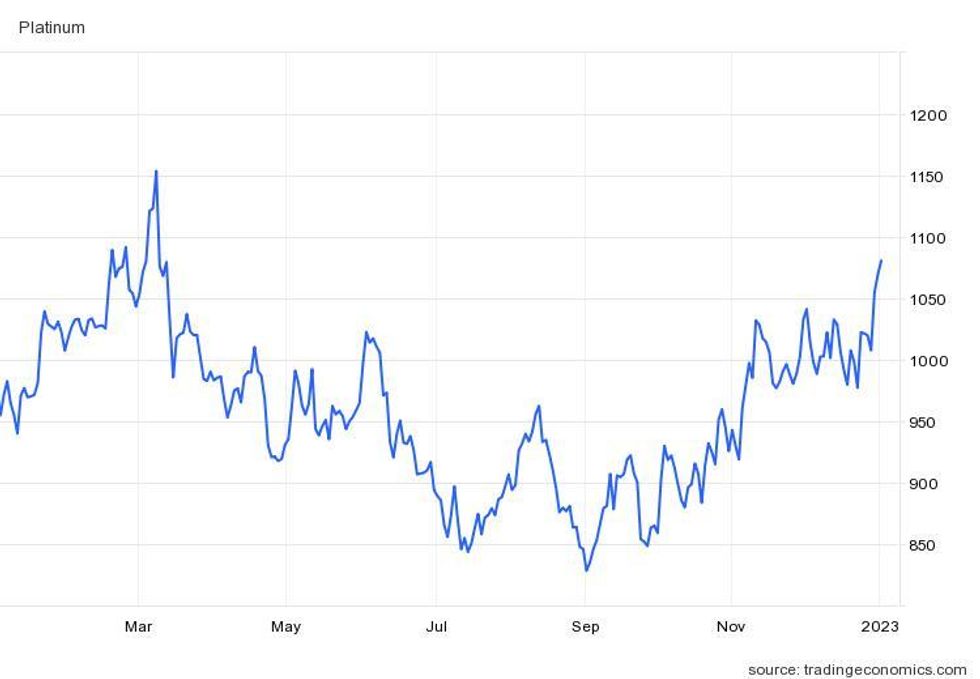

The platinum worth noticed a price spike early in 2022 following Russia’s invasion of Ukraine. Russia’s position within the platinum group metals (PGM) manufacturing area pushed the platinum worth to US$1,152 per ounce in March, its highest level since June 2021.

Concern round Russian platinum provide subsided rapidly, regardless of the nation rating second by way of annual manufacturing.

By the tip of March, costs for the treasured steel slipped again under US$1,050, the place it remained for the remainder of the 12 months.

Unable to shake off the load of worldwide financial turbulence introduced on by inflation and countering rate of interest will increase, platinum remained nicely off its 2021 excessive of US$1,303.

Platinum’s worth efficiency in 2022.

Chart by way of TradingEconomics.

Nonetheless, platinum demand did see broad development throughout demand segments serving to to scale back the platinum surplus as analysts forecast the market will swing into deficit in 2023.

“Platinum has shifted right into a small deficit this 12 months,” mentioned Wilma Swarts, director of PGM at Metals Focus. “Whereas now we have seen constructive development within the automotive sector, the underlying elements driving the market steadiness this 12 months are closely weighted in the direction of weaker provide relatively than stronger demand. World demand for 2022 will likely be flat on 2021 at 7.4 million ounces whereas international provide is forecast to say no by 11 p.c to 7.3 million ounces.”

Platinum manufacturing challenges deplete surplus

Regardless of Russian manufacturing being much less impactful to the platinum market, flooding and electrical points early in 2022 weighed on complete output for the 12 months.

“Operational challenges meant refined platinum manufacturing declined 11 p.c (-171 koz) year-on-year in Q3’22,” the World Platinum Funding Council’s platinum quarterly reads. “Upkeep and energy provide challenges in South Africa – provider of over 70 p.c of mined provide – resulted in an 18 p.c decline in the course of the quarter.”

The report pointed to Anglo American Platinum’s (LSE:AAL,OTCQX:AAUKF) rebuilding of the its Polokwane smelter and Sibanye-Stillwater’s (NYSE:SBSW,JSE:SSW) flooding at its Montana mine as main elements within the manufacturing decline.

Q3’s output discount contributed to the 9 p.c year-over-year platinum manufacturing fall.

The recycling section additionally contracted by 13 p.c or 61 thousand ounces (koz) in 2022. Fewer scrapped autocatalysts and fewer Chinese language jewellery being bought again made up the biggest portion of the shrinking section.

“Each the mining and recycling constraints are themes which can be anticipated to proceed by means of the tip of 2022 and into 2023, with complete provide for 2022 anticipated to be down 10 p.c on 2021 at 7,306 koz,” the WPIC forecast reads.

Automotive demand nonetheless recovering

By September, platinum sunk to its lowest level in nearly two years at US$828.47. The low was short-lived as costs rebounded to the US$927 degree in the beginning of the fourth quarter.

Following two years of disruptions introduced on by the pandemic, automotive demand started to recuperate in the course of the second half of 2022.

“Automotive manufacturing numbers have been constrained by the semiconductor and different provide chain challenges,” mentioned Ed Sterck, director of analysis on the WPIC. “We see these easing into subsequent 12 months. However manufacturing remains to be struggling to get again to pre-COVID ranges.”

The fragility of re-established provide chains, lingering chip shortage and the present financial setting are all headwinds that would forestall platinum worth development in 2023.

“Provided that we have had a number of years of automotive manufacturing falling under demand ranges, we have some parts of pent-up demand,” Sterck mentioned. “However even trying previous that, we predict that automotive manufacturing charges are remaining under recessionary ranges of client demand.”

On the flipside, a few of that repressed demand and the continuing substitution of palladium for platinum helped push platinum demand from the auto sector up 25 p.c year-over-year.

For Swarts, the first catalyst behind this uptick is “tighter emission” requirements.

“By mid-July (2021), all heavy-duty autos in China needed to adjust to China VIa emissions laws,” she mentioned. “Which means 2022 was the primary full 12 months during which all heavy-duty autos produced would have needed to be fitted with a China VI-compliant aftertreatment system.”

With platinum being prized for its skill to scale back car emissions, many automakers have chosen to extend platinum loadings or change expensive palladium ones with platinum.

“The substitution of platinum instead of palladium in light-duty autos ensured the demand within the light-duty section grew, regardless of the acceleration of battery electrical car manufacturing and the lingering chip and different half shortages,” Swarts mentioned.

Weak funding section outweighs robust Industrial demand

Though platinum industrial demand in Q3 rose 10 p.c in comparison with Q3 2021, general, the section contracted 14 p.c year-over-year. Nonetheless, 2021 was a file 12 months by way of industrial demand, and Sterck expects 2023 to be one other.

“There are fairly quite a few capability additions within the chemical and glass sub sectors for industrial demand, that are serving to drive 2023 to being the second strongest 12 months for industrial demand on file,” he mentioned.

The director of analysis went on to level out that Chinese language platinum imports have ballooned in recent times, just like palladium within the 2010s.

“China’s urge for food for platinum has simply skyrocketed for the reason that center of 2021,” he mentioned. “And China has been importing important quantities of platinum nicely in extra of recognized demand — about 1.2 million ounces — for the reason that starting of final 12 months.”

This might pose an issue because the market swings into deficit following a number of years of surplus.

“That materials is now graphically captured in China as a result of rules make it very troublesome, if not not possible, to export it as soon as it is within the nation,” Sterck mentioned. “So, the remainder of the world is definitely not going to have platinum to satisfy a shortfall.”

Whether or not Chinese language imports are going to the automotive sector, stockpiling or to construct the nation’s hydrogen sector is unknown. The latter is an space that Sterck sees having potential all over the world.

“There are many buyers platinum for the time being for that hydrogen angle, whether or not they really feel prefer it’s prepared for use as a proxy for hydrogen but, I feel that’s nonetheless a little bit of an open query,” Sterck mentioned. “However definitely, buyers are doing the background work now to be comfy.”

Whereas buyers look into hydrogen, the platinum ETF section continued to see outflows for the fifth consecutive quarter.

“There’s a possibility price of holding an ETF the place you are paying an annual administration payment, and any money that is related to that funding is not truly producing an revenue,” he mentioned, including that a few of the selloff has been buyers searching for yield.

Sterck went on to say that a few of the rotation out of ETFs has led buyers to the forwards and futures market the place they’ll retain publicity in a way more “price efficient vogue.”

In earlier years there has additionally been an exodus from platinum ETFs into mining equities, however 2022 was not impacted by this pattern, in line with Swarts.

“Rotation to mining equities was not a serious theme for the 575 koz liquidation now we have seen,” she mentioned. “It’s extra probably that the present inflationary considerations and rising rates of interest pushed buyers away from the dear metals advanced this 12 months.”

As ETFs confronted extra drawdowns, bar and coin demand made an incremental transfer rising by 2 p.c to 340 koz in 2022. Bar and coin purchases are anticipated to strengthen in 2023, with the bar and coin sector anticipated to make a 49 p.c uptick.

“Retail investments are sometimes good barometers of safe-haven demand and countermeasures towards rising inflation,” Swarts mentioned. “The constructive development comes from continued curiosity within the US market and our expectation of a reversal from internet promoting this 12 months to internet shopping for in Japan in 2023.”

Sterck additionally cited the Japanese market, which he described as “mature,” as a number one issue within the section’s development. After spending the early a part of 2022 promoting bars and cash, Japanese buyers pivoted and commenced shopping for once more.

“I feel that buyers in Japan have form of develop into normalized to increased worth ranges in yen phrases,” Sterck mentioned.

Manufacturing challenges persist as demand will increase

Trying additional into 2023, mining manufacturing is an element buyers ought to control in line with the WPIC.

“South Africa’s struggles with load shedding, which elevated considerably quarter-on-quarter, are anticipated to proceed to negatively impression refined steel output for the foreseeable future,” the report states. “While output from Russia is at present forecast to stay flat year-on-year in 2023.”

For Metals Focus’ Swarts, the instability in South Africa’s electrical grid is anticipated to weigh on the nation’s output.

“We can pay shut consideration to the nation’s social stability as election campaigning begins forward of the 2024 nationwide elections,” she mentioned.

The director of PGMs additionally pointed to secondary provide remaining an necessary problem this 12 months.

“This was severely impaired as fewer vehicles have been scrapped, resulting in decrease spent autocatalyst recycling,” she mentioned.

Swarts went on to say that Metals Focus can even be retaining an in depth eye on the demand facet of the market.

“The unwinding of the chip and different half shortages will stay on the radar,” Swarts mentioned. “We can even maintain shut observe of the speed of powertrain electrification and the implications of upper battery materials prices.”

Long run, the PGM specialist expects platinum’s place within the hydrogen economic system to play a job in its development.

“Developments within the funding within the hydrogen economic system will likely be necessary,” she mentioned. “Platinum will likely be a crucial uncooked materials for the manufacturing and consumption of inexperienced hydrogen.”

Platinum ended 2022 buying and selling for US$1,068.38.

Remember to comply with us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, maintain no direct funding curiosity in any firm talked about on this article.

Editorial Disclosure: The Investing Information Community doesn’t assure the accuracy or thoroughness of the data reported within the interviews it conducts. The opinions expressed in these interviews don’t replicate the opinions of the Investing Information Community and don’t represent funding recommendation. All readers are inspired to carry out their very own due diligence.

From Your Website Articles

Associated Articles Across the Internet

[ad_2]