– Funding Watch")

[ad_1]

by way of WOLF STREET:

Let me simply divert your consideration for a second from the collapse of SVB Monetary and what it would and won’t imply for the monetary system or the startup bubble or no matter, to a different troubling side of SVB Monetary that exhibits that nobody has realized something for the reason that Monetary Disaster, least of all of the credit standing businesses.

So you recognize what’s coming: The strong investment-grade score on an organization – SVB Monetary – that then collapsed with its investment-grade score, taking buyers down with it.

On Wednesday March 8, Moody’s nonetheless had an A3 score on SVB Monetary, proprietor of the now defunct Silicon Valley Financial institution, because it was already collapsing for all to see. 4 notches into funding grade – a really respectable score!

Within the night of that day, after SVB disclosed a $1.8 billion loss on the sale of bonds, a deliberate capital elevate, and a slew of liquidity measures, Moody’s downgraded it by only one itty-bitty notch, to Baa1, nonetheless three notches into funding grade.

Then on March 10, after Silicon Valley Financial institution was shut down and put into receivership, Moody’s downgraded SVB by 13 notches in a single fell-swoop, all the way in which throughout junk territory, to its lowest score, to C, which is Moody’s score for default. And it stated that it’ll withdraw the score.

That’s how nugatory these credit score rankings are in the event you depend on them in your bond holdings. However they’re good in your amusement, apparently. Right here is my cheat sheet for company bond credit score rankings by score company.

Comparable with S&P International Scores: On March 9, a day behind Moody’s, it downgraded SVB Monetary by one notch to BBB-, which continues to be funding grade.

Then on March 10, after SVB Monetary collapsed and was taken over by the FDIC, S&P slashed its score by 10 notches all through junk territory to D, for default, its lowest score.

Holders of its bonds and most popular inventory (like bonds, a legal responsibility on the financial institution’s steadiness sheet) received the rug pulled out from below them.

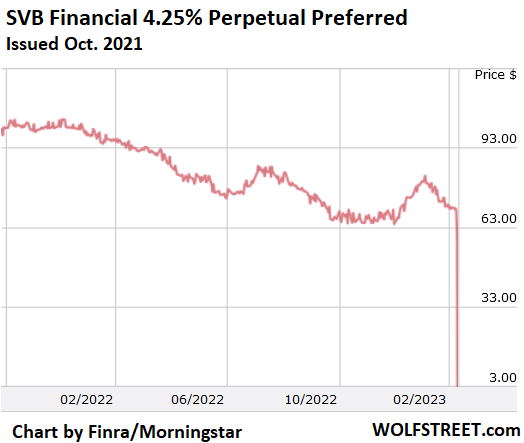

For instance, based mostly on bond knowledge from Finra-Morningstar, the $1 billion of 4.25% perpetual most popular inventory, which is able to get bailed in together with shareholders, collapsed in two days from 70 cents on the greenback to three cents on the greenback on the shut on Friday.

There are 5 issuances of this kind on its steadiness sheet that received worn out, mixed $3.7 billion. All of them had been issued throughout the Free Cash period in 2021.

The nice half for uninsured depositors is that such a debt is designed as a buffer and can get bailed in, thereby eradicating a legal responsibility from the defunct financial institution’s steadiness sheet, and leaving extra funds for unsecured depositors. So these preferreds are doing their job.

However for buyers, it could have been good to get prior warning from the credit standing businesses that these items is possibly not funding grade in any case, however junk that should include excessive yields, earlier than getting thrown off the cliff.

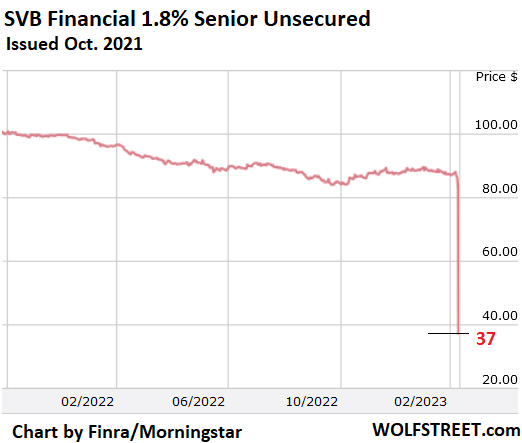

When it comes to bonds, for instance, the $650 million 1.8% senior unsecured notes, issued in October 2021, additionally throughout the Free Cash period, plunged from 86 cents on the greenback on Wednesday to 37 cents on the greenback on the shut on Friday. Traders who’d relied on the credit standing businesses to guard them from this fiasco received creamed:

Corporations clearly go ratings-shopping when they should elevate funds by issuing bonds, as a result of a decrease credit standing will trigger the bond to have a better coupon curiosity, and better yield, that means extra curiosity expense for the corporate. And so there may be big stress on analysts to give you a excessive score, or the opposite aspect of the score company will lose this enterprise to a score company that can price these bonds increased. We really have realized nothing, not even bondholders, who ought to merely ignore these rankings and do their very own homework.

[ad_2]