[ad_1]

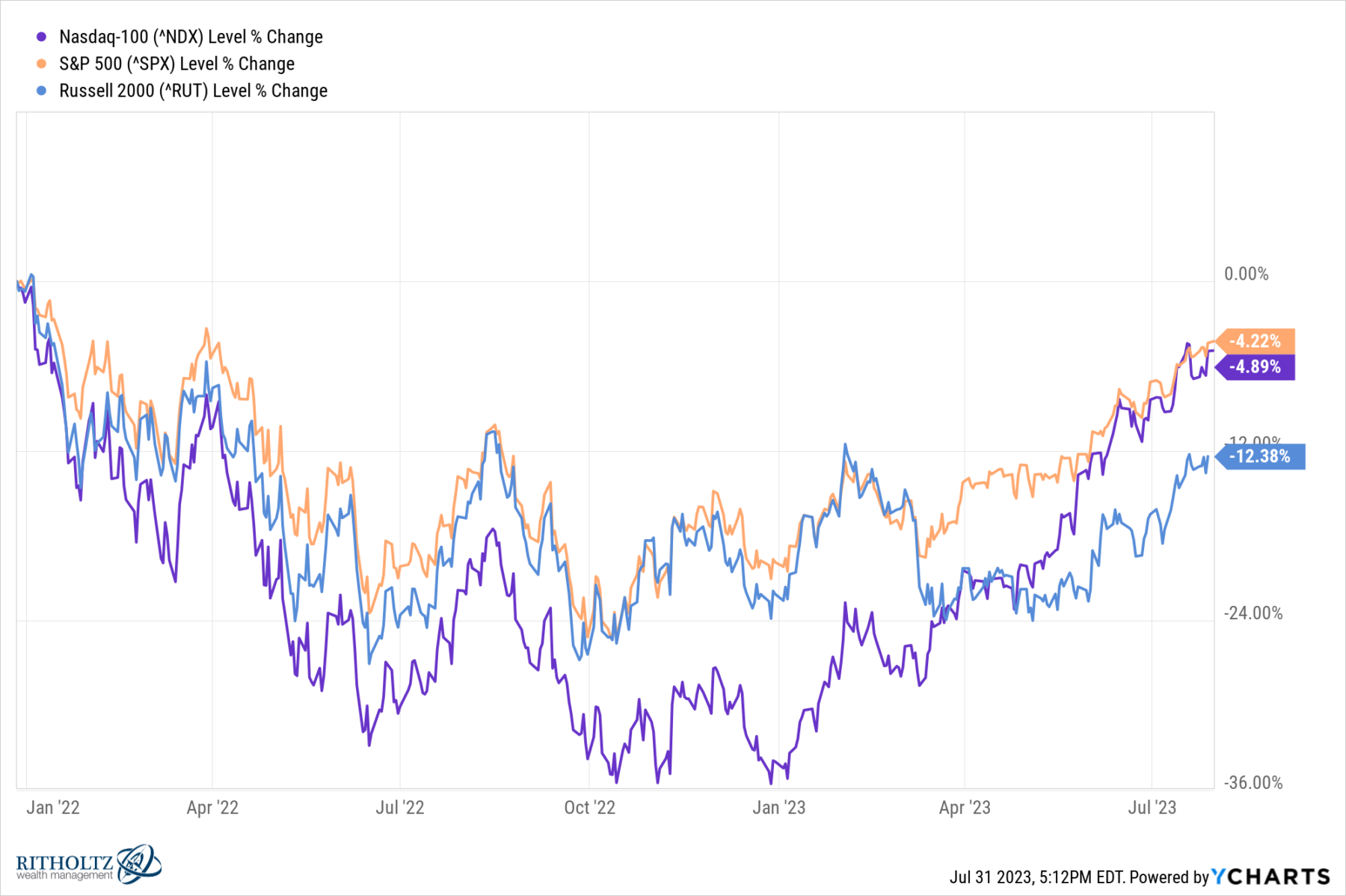

After a monstrous 68% restoration from the March 2020 pandemic low, and one other practically 30% acquire in 2021, markets determined to have one in all their all-too-regular spasms. Blame no matter you need – Too far, too quick? Finish of ZIRP? Too fast fee will increase? – however the giveback off the highs was substantial: S&P 500 was down ~23%, Russell 2000 was off 27%, and the Nasdaq 100 got here down 32%.

What a distinction a yr makes: Indices are inside spitting distance of all-time highs. Seven full months into the brand new yr, 13 months after the June lows, and 9 months after the October backside, we’ve got come all the best way again to the place we started.

In gentle of this spherical journey, it’s a good time to consider what occurred, and what we’d take from it.

The Crowd: Did the gang’s YOLO enthusiasm infect you on the best way up? Had been you a late FOMO purchaser in 2021? Did the palpable panic in June/October 2022 result in ill-advised promote(s)?

The knowledge of the gang is why the environment friendly markets work more often than not, nevertheless it actually helps to remember when the gang turns into an unthinking mob of hooligans.

Framing & Context Issues: Main indices had an infinite run within the prior decade. It’s helpful to place drawdowns of 20 or 30% into correct context once they comply with beneficial properties of 100% (SPX) and 200% (NDX).

Markets go up and down; it’s simpler to experience out a drawdown whenever you understand the giveback is a small proportion of the prior beneficial properties.

Forecasting Folly: Did you get sucked into the infinite predictions of doom and gloom? Had been you satisfied by the individuals who noticed the Recession coming?

Recall John Kenneth Galbraith’s statement: “The one operate of financial forecasting is to make astrology look respectable.”

Always remember: Forecasts are advertising.

Tech Focus: Sure, a handful of big tech shares are driving market beneficial properties. However these are usually not the profitless concepts of the dot-com period, firms like Apple, Microsoft, Google, Amazon, and so on., are fast-growing, extremely worthwhile key gamers within the fashionable financial system.

Take Apple for example: Almost $400 billion in income, $95 billion in income, 5-year income development at 11.5%, and 5-year revenue development of over 20%.

I preserve questioning why expertise is just 29% of the S&P500…

Costly Markets: There may be this fantasy that markets ought to all the time revert again to truthful worth. In actuality, that may be a level on the spectrum from low cost to pricey markets wave good day and goodbye to as they blow previous in each instructions.

Overvalued markets can keep overvalued for a lot of a bull market cycle.

Personal Credit score: An unnamed particular person from the hedge fund business identified that across the June 2022 lows, there have been large redemptions from allocators who shifted capital away from hedge funds. The explanation? They had been piling into personal credit score.

That was a crowded commerce, and it has underperformed versus equities since. However we gained’t understand how large a dropping commerce it could be till early 2024, once we see the up to date valuations. Some of us who’re extra acquainted with the numbers than I’ve prompt it won’t be fairly.

Yield Curve Inversion: Cam Harvey, the creator of this recession indicator, factors out that it’s 8 for 8 when it comes to recession forecasts. That could be a good observe document but in addition a really tiny pattern set. And it by no means has operated in an period the place charges had been at or close to zero for greater than a decade.

Some folks have argued that as a substitute of predicting recessions, an inverted yield curve really predicts the FOMC’s response to falling inflation, which may be – however isn’t all the time – related to financial contractions.

There are not any holy grails and no indicators which might be completely dependable.

Narratives & Holding Durations: Merchants have very quick holding intervals, and are involved with catalysts that drive costs short-term. Buyers maintain asset lessons, to profit from long-term worth creation and compounding.

Harm happens when narratives of merchants are used to justify the actions of traders, and vice versa.

Perceive your funding horizon, be it minutes or many years. By no means use another person’s narrative to justify your funding conduct.

Howard Marks is fond of claiming “Expertise is what you get whenever you don’t get what you need.” When you’ve got not gotten what you needed from markets for the reason that lows of 2022, then maybe you’ll find a silver lining in gaining expertise…

Beforehand:

Flawed Aspect of the Commerce (April 15, 2022)

One-Sided Markets (September 29, 2021)

Forecasting is Advertising . . . (January 24, 2015)

[ad_2]