MBW Explains is a sequence of analytical options through which we discover the context behind main music business speaking factors – and counsel what would possibly occur subsequent.

On Tuesday (March 21), world commerce physique IFPIintroduced, through its International Music Report, the official worldwide income figures for the recorded music business in 2022. These mirrored double-digit annual development in two essential areas: Subscription streaming revenues (+10.3% YoY) and total streaming revenues (+11.5% YoY).

The next day, extra excellent news: Guggenheim Companions introduced it was upgrading its inventory rating for each Warner Music Group (WMG) and Spotify (from ‘Impartial’ to ‘Purchase’), and its constructive sentiment went far past simply these two firms.

A analysis observe from Guggenheim’s Michael Morris and group acknowledged: “We imagine that the worldwide music business – together with labels, platforms and artists – has the potential for market-leading monetary development for an prolonged interval.”

In the meantime, Morgan Wallen, signed to Huge Loud however releasing beneath license to UMG’s Mercury/Republic Information, was busy reminding everybody of the facility of megastars – and of main label distribution.

Wallen’s new album, One Factor At A Time, launched March 3, bought 501,000 equal copies within the States in its first week (calculated through streaming plus gross sales), and can blast past ‘million vendor’ standing within the US by the tip of this month (per Billboard/Luminate knowledge).

So: are the heads of the key music firms pleased? Slightly, certain. For now.

However on one explicit topic, maybe greater than another, they continue to be vocally perturbed: the superabundance of music releases hitting streaming providers each 24 hours.

What’s the context?

Maybe essentially the most enlightening web page within the IFPI International Music Reportthis 12 months is the very first one within the e-book (pictured inset) – carrying succint reactions from the three heads of the majors to the present state of the market.

There’s some positivity from Sir Lucian Grainge (Common Music Group), Rob Stringer (Sony Music Group), and Robert Kyncl (Warner Music Group) in these statements. However there’s additionally a transparent name for warning concerning threats to the business’s well being.

A few of this warning is directed towards the long run potential influence of Synthetic Intelligence on music.

However the greatest observe of concern – particularly from Common and Sony’s corners – is the very-much-already-here influence of the deluge of DIY-distributed releases hitting Spotify and co. right now.

In his feedback, Common’s Grainge requires the music business to concentrate on constructing “an atmosphere through which nice music just isn’t drowned out by an ocean of noise”.

Sony’s Stringer, committing to Sony’s “top quality” output, encourages his music biz friends to stay “vigilant towards any race to the underside provided as much as shoppers”.

Readers of MBW will know precisely what Stringer means by that.

Final summer season, we quoted him explaining to Sony buyers that his firm was – primarily through its possession of The Orchard and AWAL – ”forged[ing] our nets deeper and deeper” to deliver elevated volumes of unbiased music into Sony’s distribution system.

A part of the rationale Sony’s doing this, clearly, is to battle the inevitable market share erosion that all the majors face from the glut of unbiased releases now hitting platforms.

But Stringer additionally appeared to counsel to his buyers that there was a sure minimal stage of high quality in music that Sony Music was unwilling to fall beneath, even on a distribution foundation – tracks which he memorably termed “flotsam and jetsam… simply stuff that’s taking over market share due to scale”.

MBW has reported on the downward market share influence for the majors on providers like Spotify from this flood of music earlier than.

However we’ve by no means seen stable, verified knowledge pertaining to the exact scale of the issue for the key document firms. Till now.

Final week, MBW ran a in style evaluation through which we cited a presentation from SXSW 2023 given by Rob Jonas – CEO of the leisure knowledge and insights firm, Luminate.

The section of that presentation that we cited referred to the tens of hundreds of thousands of songs presently sitting on music streaming platforms that fail to draw a single play.

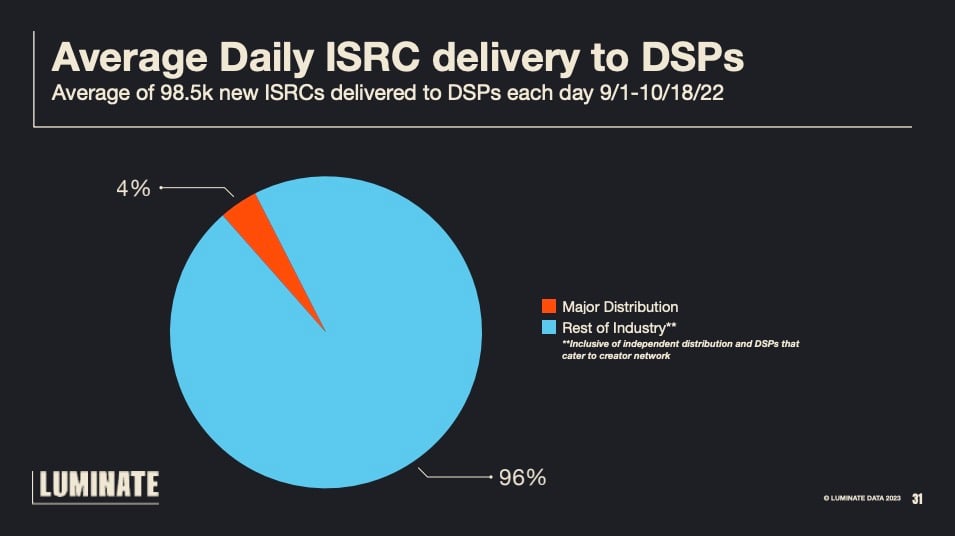

However there have been just a few extra knockout stats revealed in Jonas’ presentation, not least the one represented by the slide under.

As you possibly can see, a median of 98,500 separate music recordsdata (monitored through separate ISRC codes) have been distributed each day to audio and/or video streaming providers in the course of the interval in query (September 1 – October 18, 2022).

This tells us that the ≈100,000-tracks-per-day streaming add estimate mentioned by main music firm heads final 12 months was broadly correct.

However digging deeper into the information introduced by Jonas reveals one thing else, too: the stark numerical scale of the “flotsam and jetsam” concern for the key document firms.

Based on Luminate’s numbers, simply 4% of these 98,500 common each day observe uploads have been distributed by the three majors and/or their subsidiaries and associates.

In contrast, 96% (!) of the 98,500 tracks have been distributed by firms exterior of ‘the large three’.

To place it one other approach: The main document firms are distributing, on common, 3,940 tracks a day.

That’s a drop within the ocean in comparison with the ≈94,500 tracks being launched by ‘non-majors’ – i.e. unbiased labels and, primarily, by self-releasing/DIY artists through platforms like DistroKid, TuneCore, CD Child, and UnitedMasters.

Final twist on these numbers: For each observe launched through main document firm distribution right now, one other 24 are launched exterior their partitions.

What occurs now?

We are able to anticipate the key document firms to proceed to “widen the online”, in a bid to curb the market share injury of this development, and enhance the breadth of their unbiased artist and label distribution companies:

At Common Music Group, a new period has begun for Virgin Music Group (housing InGrooves), a united, world artist/label providers division that now sits alongside UMG’s frontline document teams as an funding precedence on the firm;

Sony Music Group continues to extend its relationship with indie expertise all over the world through The Orchard and AWAL, and just lately launched one other unbiased distribution choice through Santa Anna – a subsidiary of the (Sony-majority-owned) Alamo Information, run by Todd Moscowitz;

And at Warner, some (together with this author) anticipate to see Robert Kyncl additional empower ADA, whereas constructing on the long-held potential of Stage Music – presently the one ‘open to all’ self-upload/DIY distribution platform accessible that’s affiliated with a serious music firm.

As well as, we are able to anticipate to see the continuation of a Sir Lucian Grainge-led marketing campaign for the adoption of “artist-centric” royalty fashions at streaming providers, with the goal of financially hampering what Grainge calls “lower-quality practical music”.

For now, at the least, this campaign is essentially restricted to focusing on “dangerous actors” on streaming providers (fraudulent exercise specifically) and elevating questions round whether or not – for instance – a observe that provides nothing greater than the sound of rain falling deserves the identical royalty payout as knowledgeable recording of an artist’s unique composition.

A Last thought…

Earlier than one thing dramatic adjustments within the construction of music streaming distribution and royalties, although? This concern is just turning into extra of a headache for the majors.

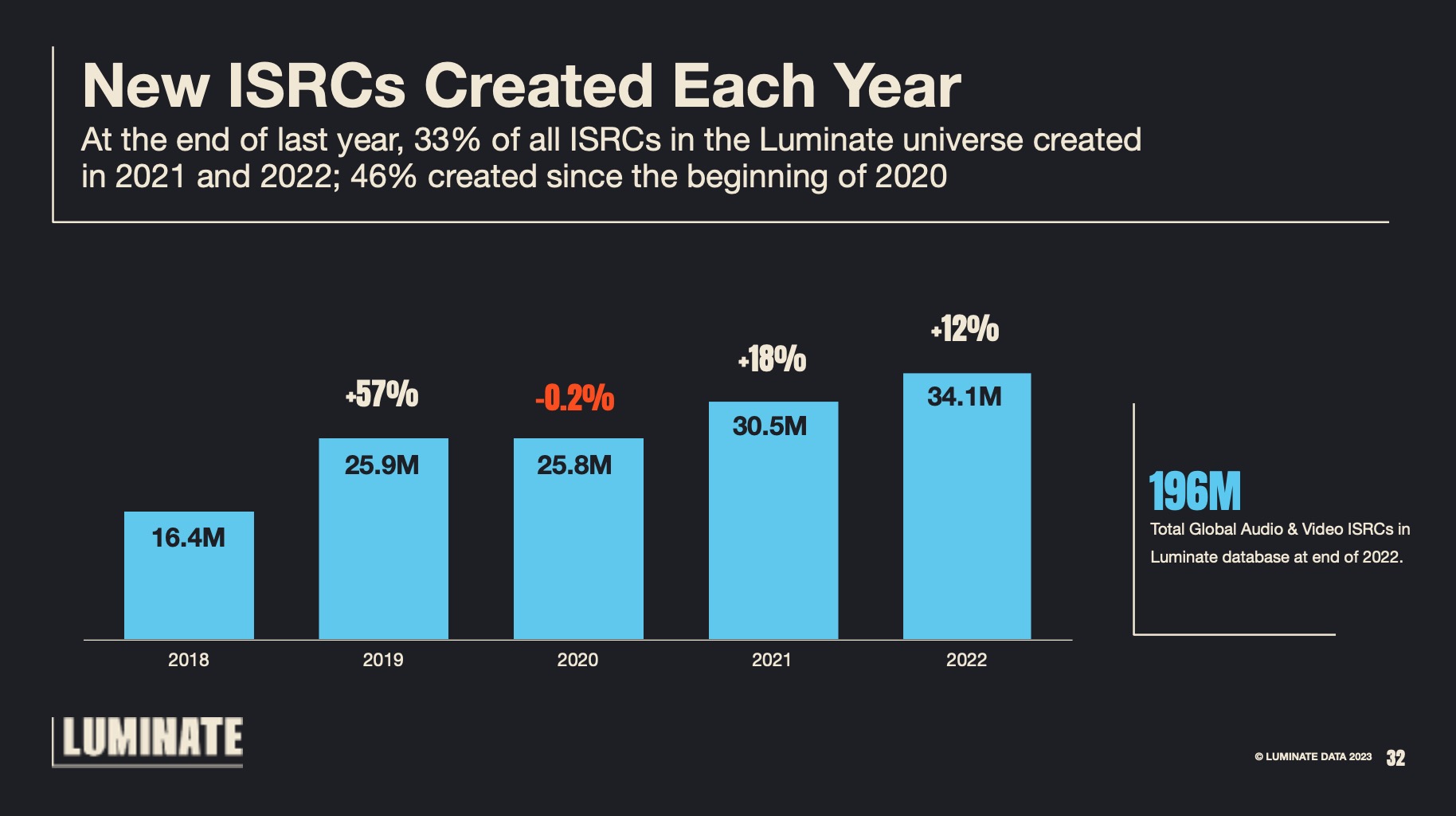

In one other slide revealed at SXSW, Luminate’s Rob Jonas revealed how the quantity of DIY artist releases has exploded lately, and exhibits no indicators of slowing down.

Right here’s the slide in query, referencing what number of audio and video music tracks (through ISRCs – Worldwide Commonplace Recording Codes) are sitting on digital providers in whole, and what number of have been created/uploaded in every of the previous 5 years.

Excluding the turbulent first pandemic 12 months of 2020, the sample is evident: Extra hundreds of thousands of tracks are being recorded and uploaded to streaming providers yearly that ticks by.

Previously three years alone, greater than 90 million separate audio or video recordings have been uploaded to streaming providers, with the most important annual haul (34.1 million) coming in 2022.

In his SXSW presentation (obtain the complete deck right here), Rob Jonas prompt that, paradoxically, the inflow of tens of hundreds of thousands of recent tracks to streaming providers could also be an element within the common streaming person’s play-count shifting in the direction of catalog, and away from newly launched music.

“In brief, when there’s an excessive amount of selection, we as shoppers can usually default to what we all know,” he mentioned.

“Just below half of all of the musical content material we’re monitoring inside our system has been created because the starting of 2020.”

Rob Jonas, Luminate

The mic-drop second, although, got here subsequent.

Jonas identified that, in response to Luminate’s knowledge, a 3rd (33%) of the 196 million audio and video music tracks on digital providers right now have been launched in both 2021 or 2022.

“And for those who add the 26 million tracks created in 2020, it signifies that slightly below half of all of the musical content material we’re monitoring inside our system has been created because the starting of 2020,” he mentioned.

“Considered one other approach, virtually half of all the music [available today was released] within the pandemic or post-pandemic period. Which is only a phenomenal, phenomenal stat.”

Right. And it’s an outstanding stat that the key document firms are taking a look at with fireplace of their eyes.Music Enterprise Worldwide