[ad_1]

A significant financial institution simply went below… contagion is dragging down different related companies… the Fed is introducing emergency measures to bailout the system.

Is it 2008 yet again?

Sure and no.

“Sure” within the sense that the Fed created an enormous bubble in danger property. Additionally “sure” within the sense that banks made silly choices, violating central tenets of danger administration by lending cash to purchasers that would by no means pay it again (this time tech startups as an alternative of excessive danger mortgage debtors). And eventually “sure” within the sense that the responsible gamers get bailed out by the tax-payer and the rich are made “entire” with preferential therapy because of their connections to DC.

Nonetheless, that’s the place the similarities finish… as a result of the problems the monetary system faces at present are far larger and systemic that those it confronted in 2008.

The 2008 disaster was triggered by a disaster in housing… which grew to become a banking disaster courtesy of Wall Avenue’s poisonous derivatives trades,

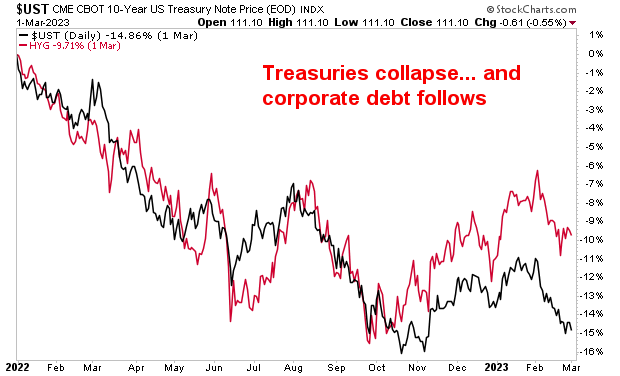

This disaster (2023) is a disaster in Treasuries… that are the bedrock of our present monetary system, the senior-most asset class in existences. And as soon as once more Wall Avenue has gone bananas with derivatives primarily based on an asset class.

In 2008, the derivatives have been “credit score default swaps” and the marketplace for them was roughly $50-$60 trillion in measurement.

As we speak, the derivatives are primarily based on “rates of interest/ bond yields” and the marketplace for them is $500+ trillion. And as we simply found with Silicon Valley Financial institution and Signature Financial institution… the banks weren’t significantly intelligent in how they managed their dangers this time both.

Over the past yr because the Fed raised rates of interest from 0.25% to 4.75%, the Treasury market has collapsed. Keep in mind, when bond yields RISE, bond costs FALL.

Different debt securities adopted swimsuit together with mortgage-backed securities, company bonds and the like. As a result of bear in mind, the yield on Treasuries represents the “danger free” fee of return towards which all danger property are priced. So when Treasuries fell, ALL different debt devices needed to be repriced accordingly.

Because of this, U.S. banks are at the moment sitting on $640 BILLION in unrealized losses on their longer length bond/debt portfolios. That is what precipitated the collapse of Silicon Valley Financial institution… and should you assume that’s the final shoe to fall on this mess, I’ve received a bridge to promote you in Brooklyn.

So benefit from the bounce we’re seeing in danger property now. It gained’t final… simply because the market rally triggered by Bear Stearns’ shotgun marriage ceremony to JP Morgan in March 2008 didn’t final both.

Certainly, from a BIG PICTURE perspective my proprietary Crash Set off is now on the primary confirmed “Promote” sign since 2008.

This sign has solely registered THREE instances within the final 25 years: in 2000, 2008 and at present.

In the event you’ve but to take steps to arrange for what’s coming, we simply revealed a brand new unique particular report Easy methods to Make investments Throughout This Bear Market.

It particulars the #1 funding to personal throughout the bear market in addition to learn how to make investments to probably generate life altering wealth when it ends.

To select up your FREE copy, swing by:

phoenixcapitalmarketing.com/BM.html

PS. Our new investing podcast Bulls, Bears & BS is formally reside and out there on each main podcast utility (Apple, Spotify, and many others.)

To obtain or hear, swing by:

[ad_2]