[ad_1]

Jerome Powell and the Federal Reserve spend loads of time worrying about Inflation Expectations.

They shouldn’t.

Usually, Sentiment Surveys are ineffective — more often than not — the exception being on uncommon events on the extremes.

They aren’t merely lagging, backward-looking indicators, however as an alternative, inform us as to what the general public was experiencing about 3-6 months in the past. Sometimes, it takes individuals just a few weeks or months to subconsciously incorporate broad, refined modifications into their inside psychological fashions, and longer to consciously acknowledge these nuanced shifts.

Past short-term pattern extrapolation, inflation expectations have little to no capability to supply perception into the intermediate-future (e.g., 6-12 months) inflation. As to the longer-term, the 5-Yr Ahead Inflation Expectation Fee are ridonkulously, hilariously, laughably ineffective. They’re so foolish as to be “Not even fallacious” — simply goofy irrelevant guesses.

Right here is Brookings explaining the origins of inflation expectations:

“Central bankers’ deal with inflation expectations displays the emphasis that tutorial economists, starting within the late Nineteen Sixties (together with Nobel laureates Edmund Phelps and Milton Friedman), placed on inflation expectations as key to the connection that ties inflation to unemployment.”

So, the pre-globalization, pre-automation, and pre-behavioral finance analog period of the Nineteen Seventies is the driving force of this indicator. This explains partially why it’s largely ineffective. And but, regardless of that, individuals with necessary jobs nonetheless give it weight. Because the close by charts clarify, they shouldn’t.

We’ve mentioned the issues of forecasting sufficient up to now that I gained’t spend an excessive amount of time right here, apart from to level out that people as a species haven’t any thought what’s going to occur in a month or 3, a lot much less 5 years therefore.

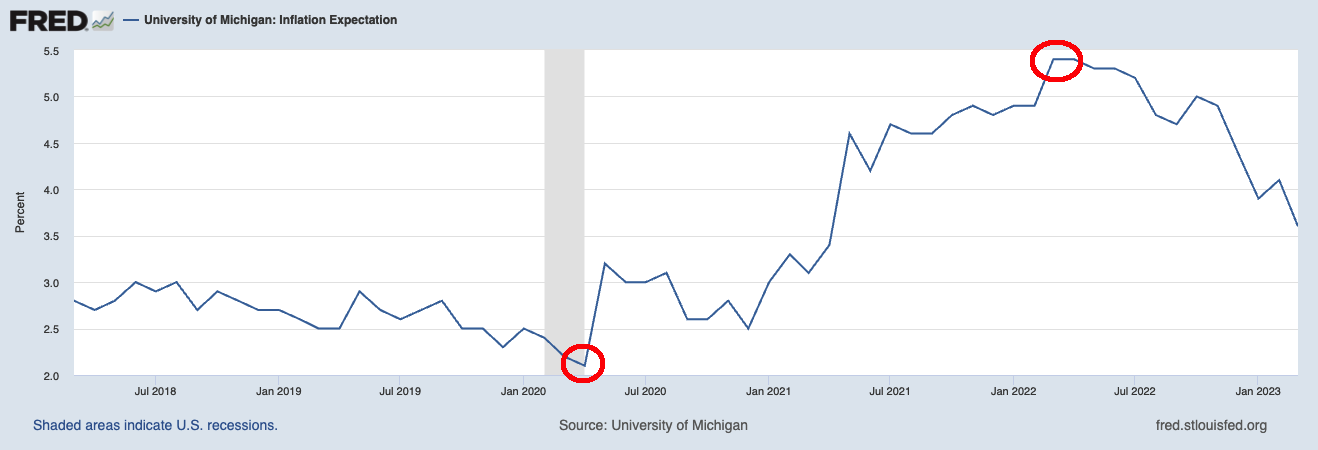

Extra particularly, as a bunch, individuals get issues like inflation expectations exactly backward: Their expectations of inflation are on the very LOWEST proper earlier than a spike in inflation is about to happen. As if that wasn’t unhealthy sufficient, their expectations of inflation are on the very HIGHEST proper earlier than inflation peaks and rolls over.

The FRED chart at prime exhibits the excessive and low of the College of Michigan Inflation Expectations Survey in the course of the pre- and post-pandemic period (2018-2023).

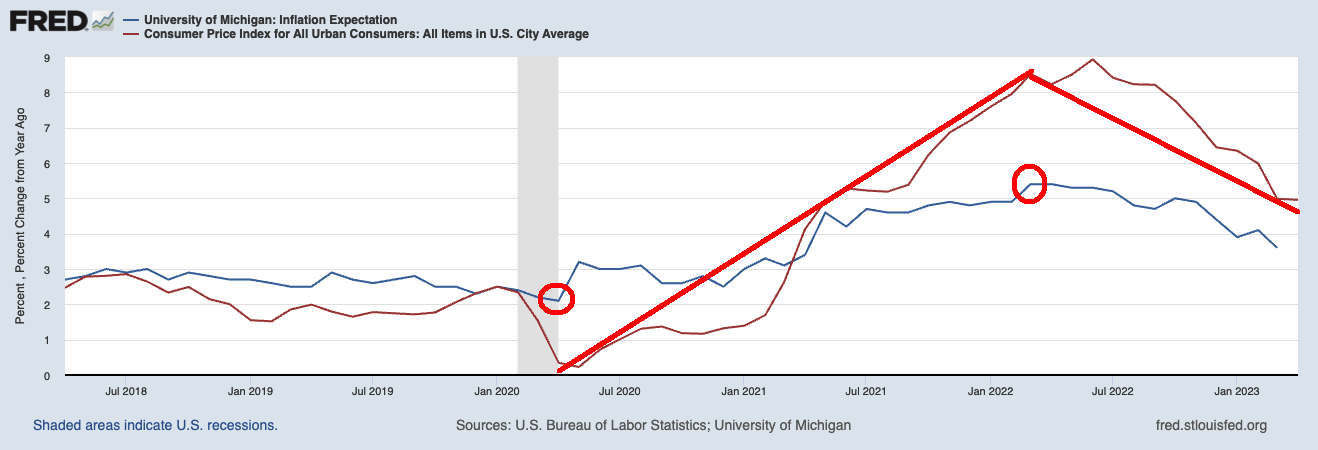

To make this clearer, let’s overlay year-over-year CPI modifications1 on Inflation Expectations:

As you possibly can see, expectations bottomed in early 2020, simply as CPI started its epic run-up into double digits a few yr later.

And as Inflation Expectations plateaued on the peak of inflation knowledge, guess what occurred to CPI over the following months?

Annualized inflation:

July 8.52%

Aug 8.26%

Sept 8.20%

Oct 7.75%

Nov 7.11%

Dec 6.45%

Jan 6.41%

Feb 6.04%

March 4.98%

April 4.93%.

As you’d anticipate,2 expectations peaked, simply earlier than it started an epic collapse, particularly in items inflation.

Anybody who desires to make use of Inflation Expectations as an indicator is welcome to — simply as long as you acknowledge that at its excessive readings, it really works finest as a CONTRARY INDICATOR…

UPDATE: Could 17, 2023

We’re directed to a current Fed paper that makes the identical level however from a unique perspective:

“Economists and financial policymakers consider that households’ and corporations’ expectations of future inflation are a key determinant of precise inflation. A evaluation of the related theoretical and empirical literature means that this perception rests on extraordinarily shaky foundations, and a case is made that adhering to it uncritically may simply result in severe coverage errors.”

See additionally:

Why Do We Assume That Inflation Expectations Matter for Inflation? (And Ought to We?)

Jeremy B. Rudd

Federal Reserve Board* September 23, 2021.

Beforehand:

2000: “Irrespective of how you narrow it, you’ve bought to personal Cisco” (Could 15, 2023)

Can Anybody Catch Nokia? (October 26, 2022)

Steadily, Then Out of the blue (October 1, 2021).

Why the Apple Retailer Will Fail (Could 20, 2021)

No person Is aware of Nuthin’ (Could 5, 2016)

How Information Appears When Its Outdated (October 29, 2021)

__________

1. As a result of the CPI swing is so giant, it compresses expectations) makes the expectations portion seem compressed

2. That checklist is by way of my colleague Ben Carlson

[ad_2]