[ad_1]

The transient’s key findings are:

- Our 2023 Small Enterprise Retirement Survey appears at why some small corporations supply a retirement financial savings plan and others don’t.

- Components that have an effect on whether or not small corporations supply a plan embody agency measurement, wages, and business, in addition to beliefs on whether or not it is going to assist appeal to employees.

- The primary obstacles to providing a plan are issues concerning the stability/measurement of the agency and the perceived prices of a plan.

- Considerations about prices are pushed by misperceptions; many corporations are unaware of lower-cost choices for employers and tax credit.

- The outcomes additionally counsel that state auto-IRA applications usually tend to encourage than discourage corporations from providing their very own plan.

Introduction

At any given time, solely about half of U.S. personal sector employees are lined by an employer-sponsored retirement plan, and few employees save with out one. The protection hole, which undermines the retirement safety of the nation’s employees, is pushed by a scarcity of protection amongst small employers. Apparently, nevertheless, about half of corporations with lower than 100 workers do supply a plan for his or her workers. This transient, which is predicated on a latest examine, presents the outcomes of a brand new survey of small employers to know why some supply retirement plans and others don’t.

The dialogue proceeds as follows. The primary part describes the brand new survey and identifies elements that make a agency doubtless to offer protection. The second part reviews the obstacles that corporations understand to providing a plan and assesses the accuracy of those perceptions. The third part examines whether or not the presence of state-sponsored retirement applications – which typically require corporations and not using a plan to enroll their employees within the state program – shifts agency perceptions.

The ultimate part concludes that essential drivers to providing a plan, presently or within the close to future, are a agency’s beliefs, reminiscent of whether or not they suppose retirement plans matter for worker hiring and retention. Importantly, many employers and not using a plan maintain misperceptions concerning the monetary and time prices of providing one. Subsequently, higher consciousness of the various obtainable choices for small corporations could assist shut the protection hole. Lastly, state-sponsored retirement applications usually tend to encourage than discourage the adoption of employer plans.

The 2023 Small Enterprise Retirement Survey

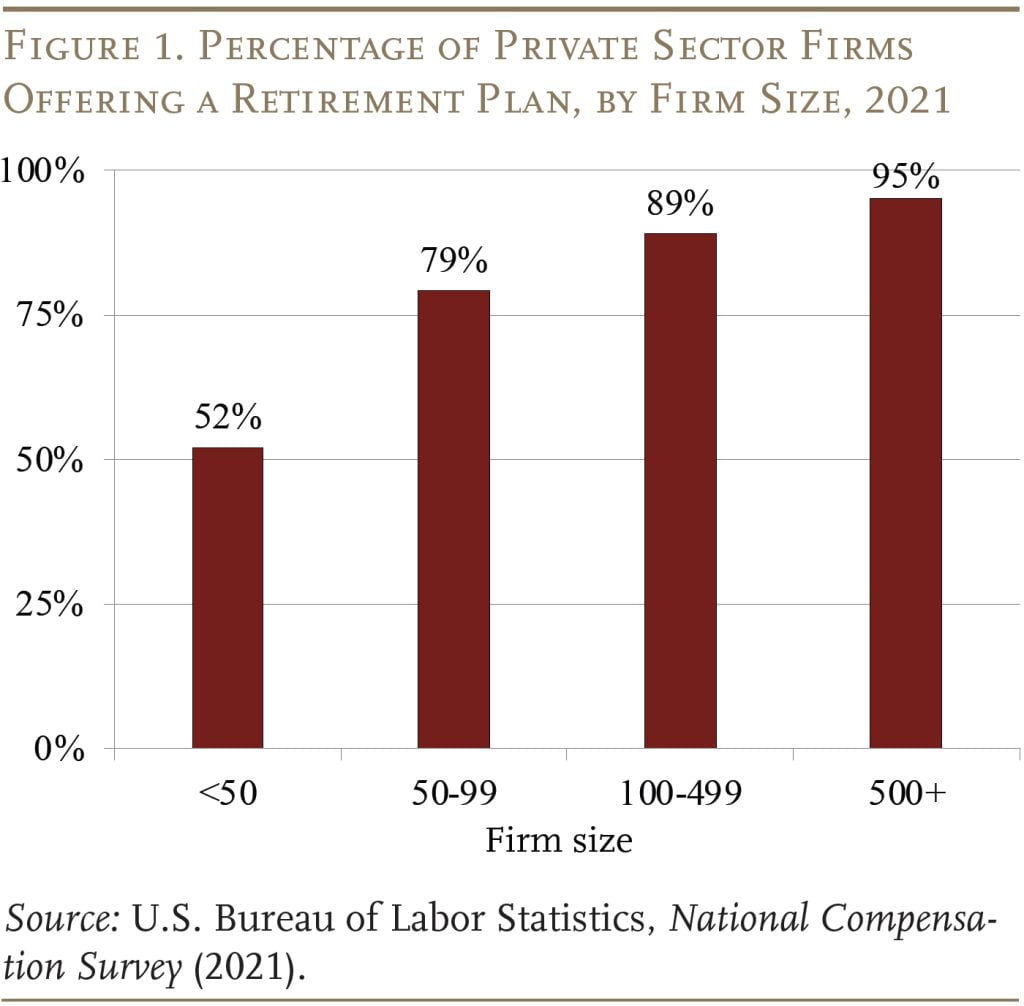

The 2023 Small Enterprise Retirement Survey, which was produced in collaboration with the Worker Profit Retirement Institute (EBRI) and Greenwald Analysis, was carried out between February and April 2023 and contains 703 corporations with 100 or fewer workers. This survey replicates the final main survey targeted on small enterprise retirement plans, which was carried out in 1998 by EBRI and Greenwald Analysis. What is exclusive concerning the 2023 survey is that it features a pattern of 100 corporations with 0-4 workers – a bunch often excluded from surveys of small employers. Amongst all corporations sampled, 46 % supplied a retirement plan, whereas the opposite 54 % didn’t. Since 92 % of all small corporations have fewer than 20 workers, this sample is pretty according to nationwide knowledge (see Determine 1).

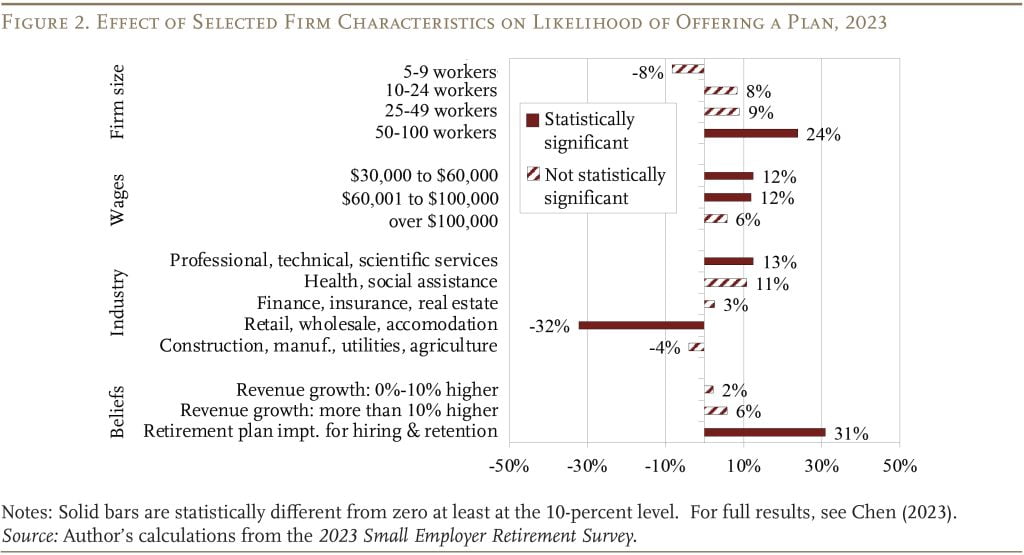

The survey responses can relate varied elements to the probability of a agency providing a plan (see Determine 2). As anticipated from earlier research, corporations with 50-100 workers, these with larger common salaries, and corporations in skilled, technical, and scientific providers industries are more likely to supply a retirement plan. In the meantime, corporations in retail gross sales, wholesale gross sales, and lodging (hospitality and meals providers) are a lot much less prone to supply a plan. However different elements additionally mattered. Beliefs about whether or not having a retirement plan is essential for hiring and retaining good workers are additionally a robust driver. Notably, a agency’s beliefs about income development had little to no impact on having a retirement plan. Apparently, for corporations and not using a plan, beliefs are additionally an essential predictor of their probability of adopting a plan within the close to future.

What Retains Corporations from Providing a Plan?

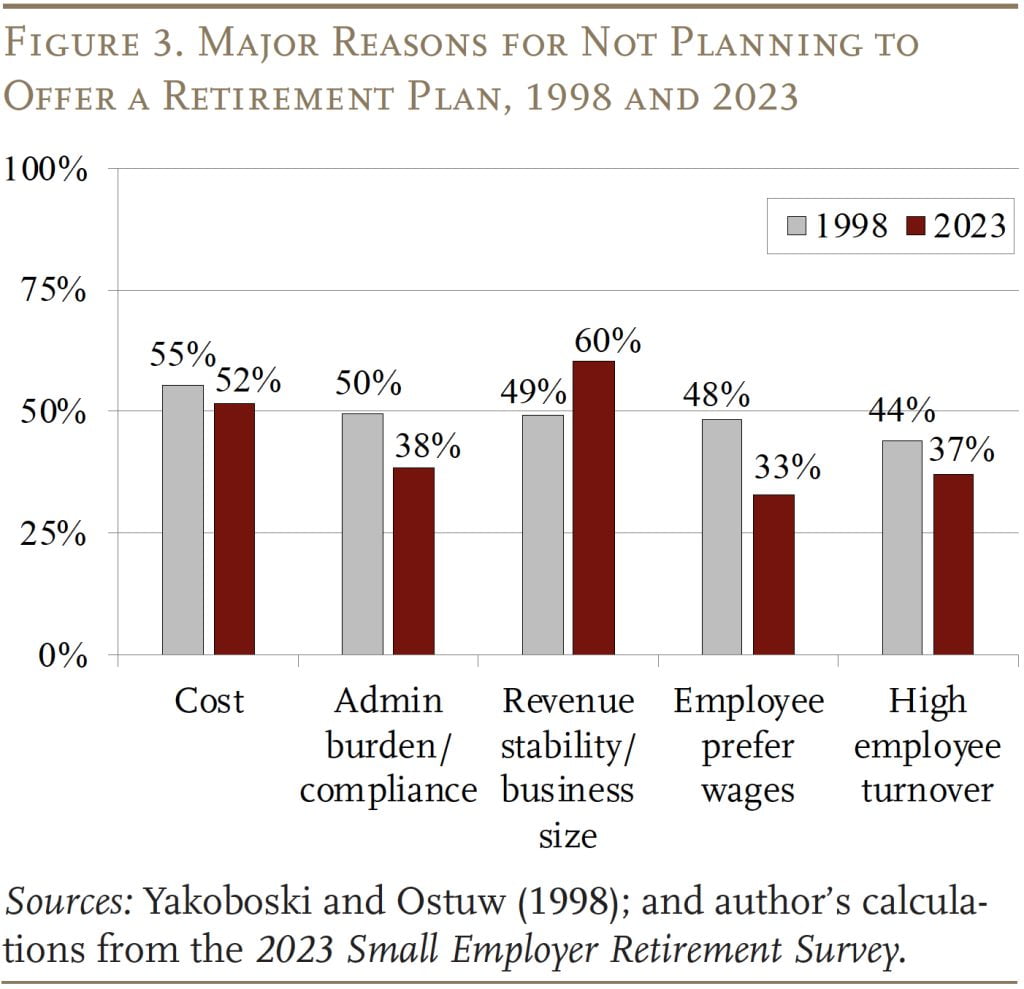

Traditionally, small corporations that don’t supply a plan have cited three important causes: 1) unsure revenues; 2) prices; and three) worker preferences for wages. The third purpose, worker preferences for wages, has dropped down the record, however prices stay essential, whereas issues about income stability/measurement have grown to grow to be the largest barrier (see Determine 3).

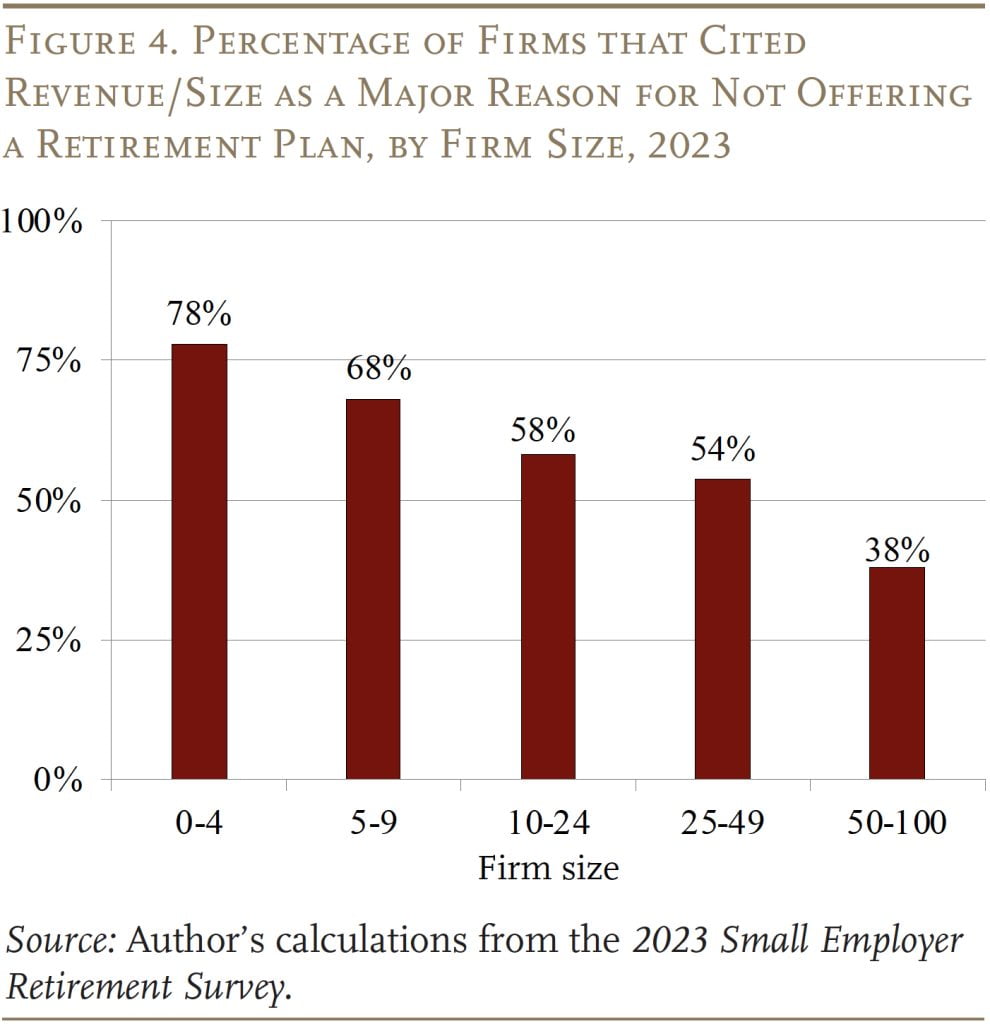

As one would anticipate, concern about revenues declines as agency measurement will increase (see Determine 4). Certainly, near 80 % of corporations with 0-4 workers cited income and measurement as a serious barrier to providing a plan. The smallest of those small corporations could merely have an excessive amount of on their plate so as to add a further profit. For established corporations, prices and administrative burdens grow to be crucial issue for not providing a plan.

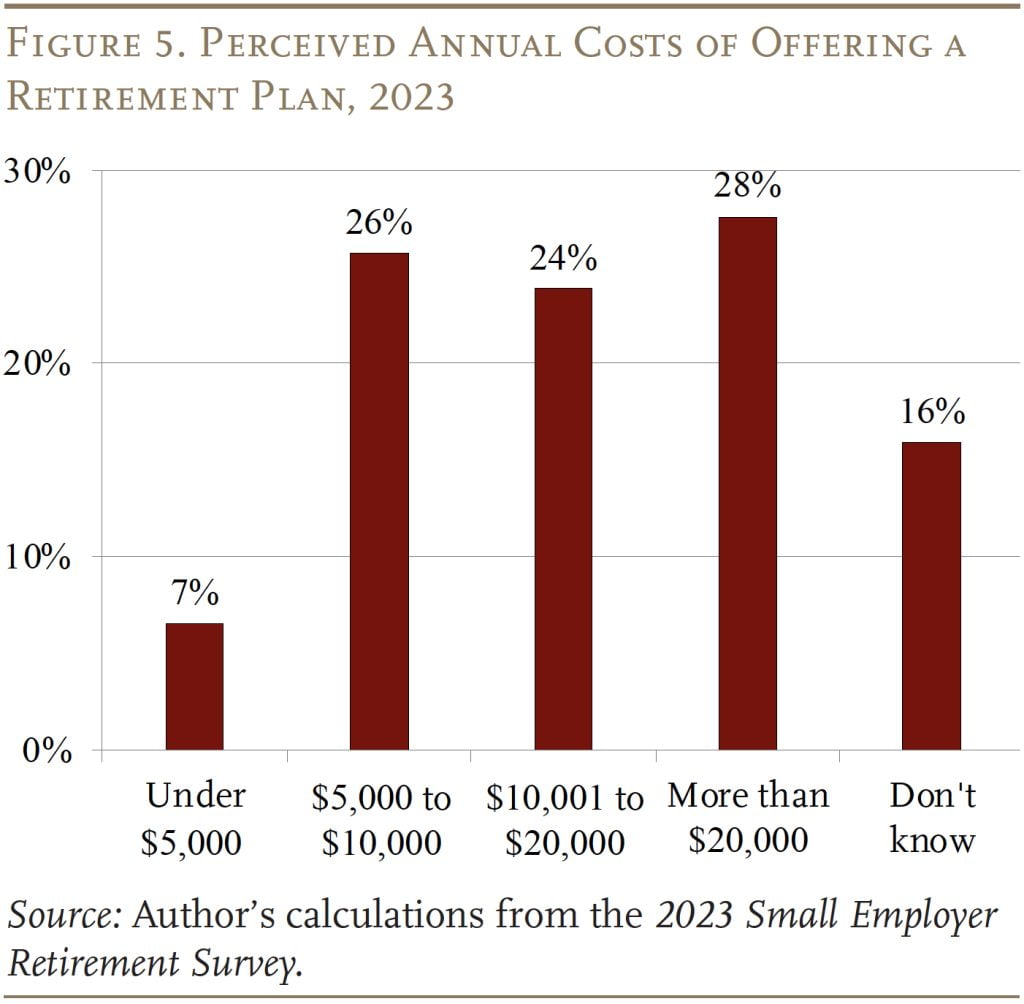

Apparently, most corporations surveyed that cite prices and administrative burden/compliance as obstacles should not have a great sense of how a lot cash or time is definitely required to arrange a plan. A fast Google search yielded a number of 401(ok) choices the place annual employer prices would solely be about $2,500 for a agency with 10 workers and $5,000 for a agency with 50 workers. However, over half of small corporations consider offering a retirement plan would price greater than $10,000 per yr; and practically 30 % suppose it might price greater than $20,000 per yr (see Determine 5).

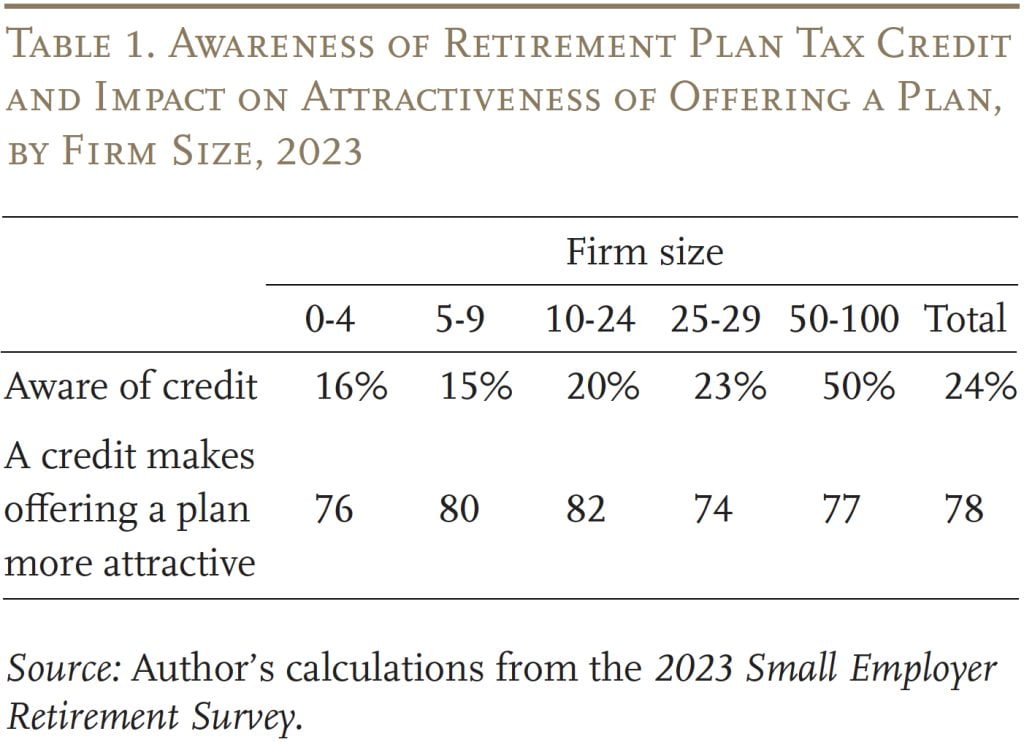

Not solely do small corporations overestimate the price of providing a plan, however the overwhelming majority – notably these with fewer than 50 employees – usually are not conscious that they’ll declare a tax credit score of as much as $5,000 for 3 years to assist offset the prices of beginning a plan (see Desk 1). Apparently, about 80 % of employers say that such a credit score would make providing a plan extra enticing.

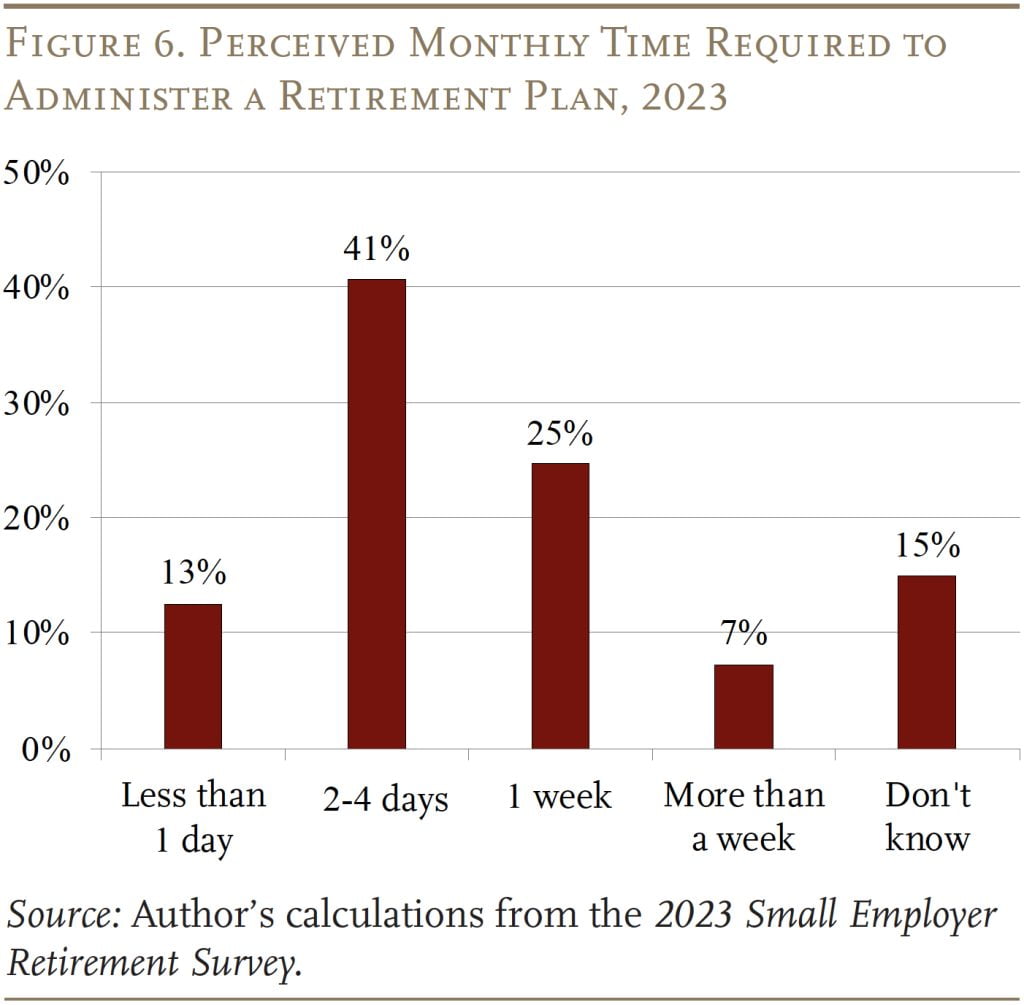

Moreover, small corporations should not have a great sense of how a lot time it might take to manage a retirement plan (see Determine 6). Most corporations consider it might take a number of days to an entire week each month. However in actuality, after the preliminary set-up, working a retirement plan ought to solely take a number of hours a yr.

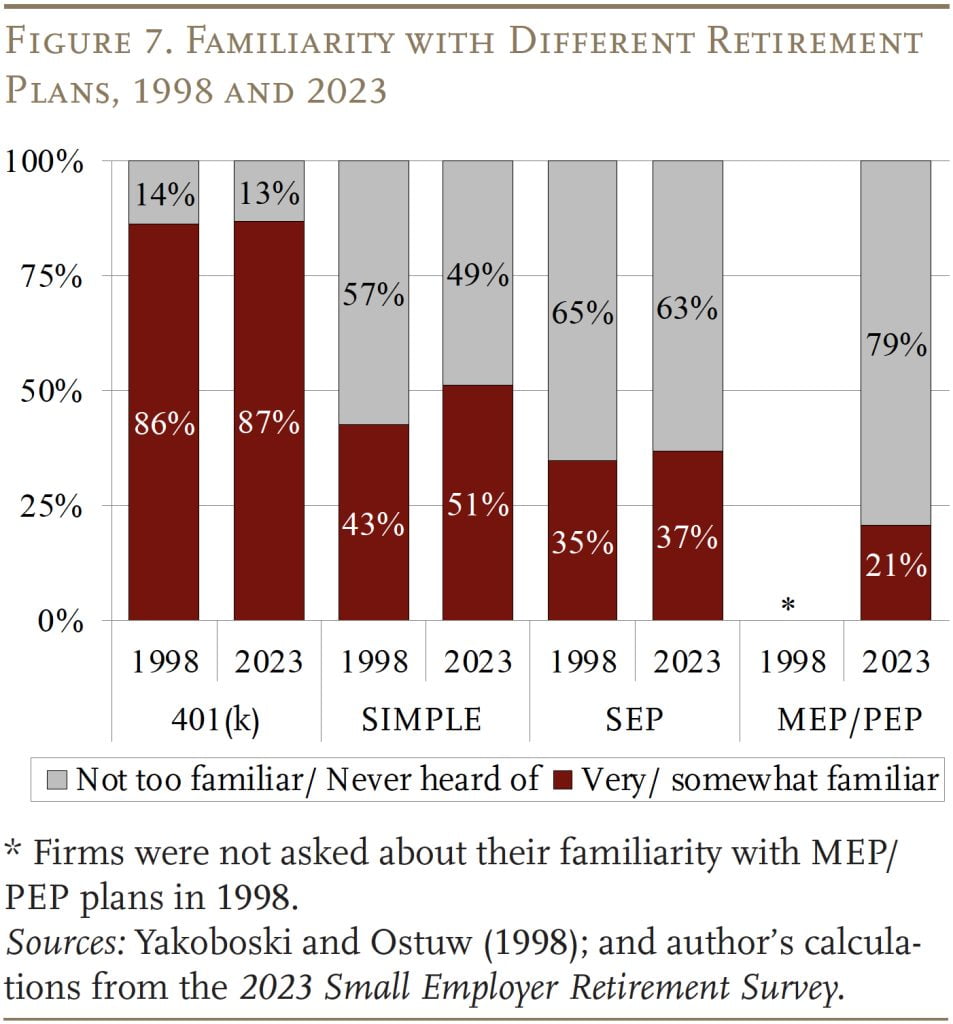

Many small corporations are additionally unfamiliar with the assorted retirement plan choices which are designed to assist ease the fee and administrative burden of providing a plan. Whereas most small corporations are not less than considerably aware of 401(ok)s, the overwhelming majority usually are not aware of SIMPLE, SEP, and MEP/PEP plans (see Determine 7). And this proportion has barely budged within the final 25 years.

These outcomes counsel that many corporations overestimate the monetary and time prices required to supply a plan, so higher consciousness of precise prices in addition to obtainable choices may assist cut back the obstacles that small corporations understand.

Will State-sponsored Packages Impression Agency Habits?

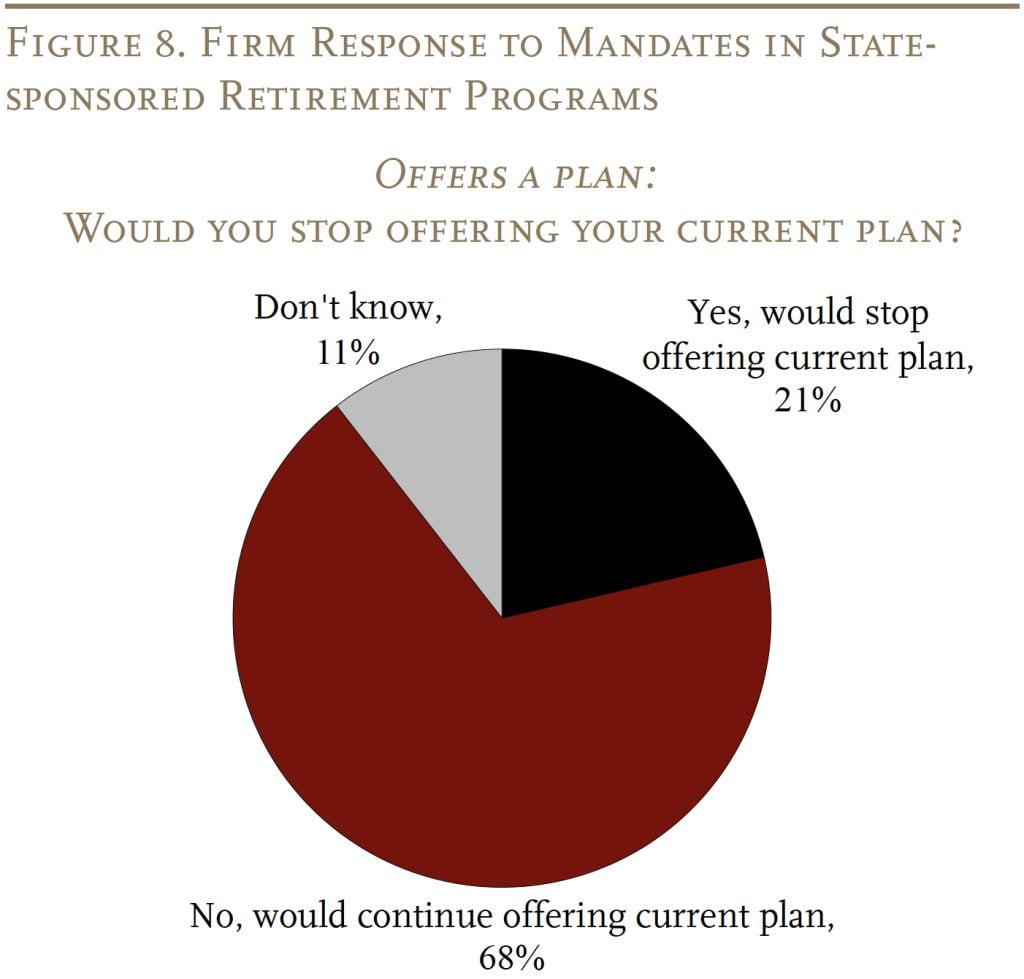

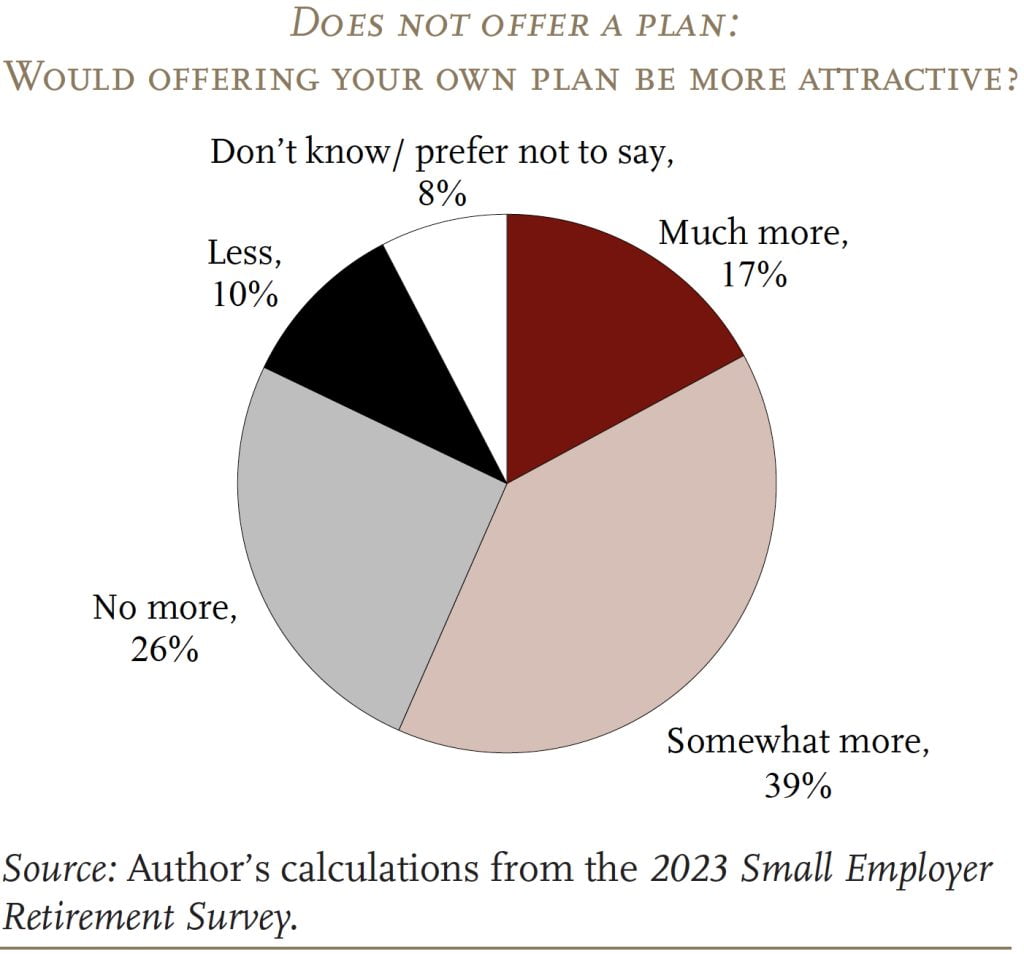

At present, 14 states have launched or are making ready to launch applications requiring employers and not using a plan to mechanically enroll their workers in an Particular person Retirement Account (“auto-IRAs”). The survey requested all employers within the pattern – not simply these in states with auto-IRAs – whether or not the presence of such a program would make them much less or extra prone to have their very own plan.

The outcomes present that, general, the presence of state-sponsored applications doesn’t make corporations much less prone to supply their very own retirement plan (see Determine 8). Amongst corporations that already supply a plan, about 70 % say they’d proceed to supply their very own if their state launched a mandate. Amongst corporations that didn’t supply a plan, nearly 60 % stated a mandate would truly make providing their personal retirement plan extra enticing.

Conclusion

The protection hole is a urgent concern for the nation’s retirement revenue safety, and the hole is pushed by small employers. With the intention to encourage development in protection, it is very important perceive the traits of small corporations that do and don’t supply a plan.

For corporations that supply or are contemplating providing a retirement plan within the close to future, their beliefs are essential – reminiscent of whether or not they suppose retirement plans matter for worker hiring and retention.

For corporations that don’t supply a plan, two main longstanding obstacles – income stability/measurement and prices or administrative burden of getting a plan – stay prime issues amongst small corporations as we speak.

Income issues are extremely related to agency measurement, notably corporations with fewer than 10 workers. It’s comprehensible that corporations could have to grow to be established earlier than establishing a office retirement plan is seen as a viable choice.

Views on price or administrative burdens, nevertheless, appear to be pushed by misperceptions concerning the monetary prices and the time it might take to function a plan. These outcomes counsel that higher consciousness of the particular prices in addition to plan choices designed for small corporations may assist cut back the obstacles that small corporations understand.

Lastly, the expansion of state-sponsored retirement applications may very well encourage corporations and not using a plan to undertake one.

References

Bloomfield, Adam, Kyung Min Lee, Jay Philbrick, and Sita Slavov. 2023. “How Do Corporations Reply to State Retirement Plan Mandates.” Working Paper 31398. Cambridge, MA: Nationwide Bureau of Financial Analysis.

Heart for Retirement Analysis at Boston School, Worker Profit Analysis Institute, and Greenwald Analysis. 2023. 2023 Small Employer Retirement Survey.

Chen, Anqi. 2023. “Small Enterprise Retirement Plans: The Significance of Employer Perceptions of Advantages and Prices.” Particular Report. Chestnut Hill, MA: Heart for Retirement Analysis at Boston School.

Drobleyn, Eric. 2023. “How A lot Time Does Annual 401(ok) Administration Take?” Cell, AL: Worker Fiduciary.

Guzoto, Theron, Mark Hines, and Allison Shelton. 2022. “State Auto-IRAs Proceed to Complement Personal Marketplace for Retirement Plans.” Washington, DC: Pew Charitable Trusts.

U.S. Bureau of Labor Statistics. Enterprise Employment Dynamics, 2022. Washington, DC.

U.S. Bureau of Labor Statistics. Nationwide Compensation Survey, 2021. Washington, DC.

Yakoboski, Paul and Pamela Ostuw. 1998. “Small Employers and the Problem of Sponsoring a Retirement Plan: Outcomes of the 1998 Small Employer Retirement Survey.” Subject Transient Quantity 202. Washington, DC: Worker Profit Analysis Institute.

[ad_2]