[ad_1]

There was a glimmer of hope within the housing information from January. The inventory market rallied sharply and there was loads of commentary about how the financial system is headed again to growth time. I’m not so assured and I nonetheless firmly consider that the “muddle via” situation I discussed in my full 12 months outlook is the baseline. And I might argue that the uneven threat to this outlook is to the draw back, not the upside.

Housing is the Economic system.

I hesitate to attribute financial development solely to 1 sector, however the US housing sector is so giant that it has a disproportionately giant affect on baseline development. So when housing strikes lots in a single route or the opposite it has a disproportionate affect on mixture development. This was the fundamental gist of the well-known Ed Leamer paper which was revealed in 2007 earlier than all of us realized this was all too true.

I formally turned bearish on housing in April of 2022. The fundamental gist of my view was that housing costs had change into unhinged from fundamentals and rising rates of interest decreased affordability to an extent that will considerably cut back demand. That is trying fairly good as far as home costs peaked final Summer season and all of the housing information has crashed since, however I don’t suppose it has totally performed out.

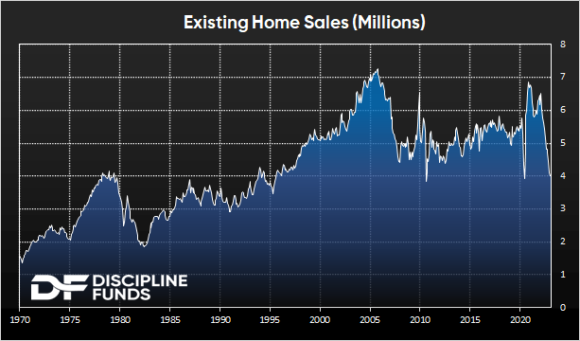

Housing information has turned very damaging in latest months. A number of the information is shockingly unhealthy. Current dwelling gross sales are at ranges final seen in the course of the COVID low and Nice Monetary Disaster.

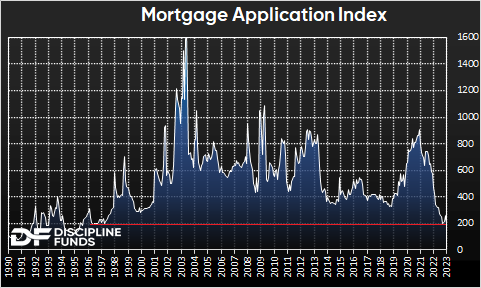

It’s tempting to have a look at information like this and assume that it’s nearer to the underside than the highest (which might be a great factor). However it’s laborious to see how this recovers considerably as a result of the affordability situation is the principle driver in housing demand. And housing affordability is nowhere close to the place it must be for demand to come back again. We had been reminded of this this morning when the mortgage software information was launched. After a short respite final month the most recent launch confirmed a brand new low. A low we haven’t seen in virtually 30 years.

That is breathtaking information. However home costs haven’t actually budged all that a lot but. Sure, we’re beginning to see actual indicators of strain in some greater tier markets like San Francisco (the place costs are already off 10%+), but it surely hasn’t been all that broad up to now. But when I had to make use of the previous baseball analogy I’d say we’re in in regards to the 4th inning of this sport and the pitcher wants reduction.

The affordability equation is a reasonably easy one. Home costs are too excessive relative to mortgage charges. And rents vs home costs are as large as they’ve ever been. So renters who’re enthusiastic about shopping for usually tend to preserve renting. And homeowners who need to transfer will hold onto their “golden handcuffs” with a low mortgage till issues change. So we want both an enormous adjustment decrease in rates of interest, an enormous decline in costs or the almost definitely situation is that we finally get some mixture of the 2.

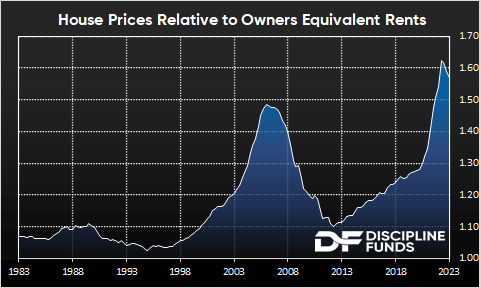

For perspective, right here’s the hire vs worth information. This information is very imply reverting as a result of folks should dwell someplace and the relative value of renting vs shopping for is likely one of the most important drivers in housing demand. We frequently hear that stock is low on this market and meaning home costs can’t fall, however this ignores the truth that folks can select to hire. And the mathematics on shopping for vs renting at current is fairly black and white – renting is much extra inexpensive.

Essentially the most troubling side of this information is simply sizzling out of whack it stays. Rents have elevated considerably lately, however home costs haven’t come down a lot. In order that both implies that rents have to maneuver a lot greater or home costs want to come back down lots. Or, some combo of the 2.

The issue is that if rents proceed to rise considerably that may bleed into inflation information as a result of shelter is such a big part of inflation metrics. Which suggests the Fed will stay greater for longer. Which implies that demand for housing will stay weak. However, many real-time rental metrics are exhibiting indicators of slowing which might imply that the long run reversion is almost definitely to come back from worth declines. So it’s laborious to place collectively a situation the place dwelling costs don’t have a come-to-Jesus second in some unspecified time in the future within the coming years. The one query is when?

In fact, the outlier Goldilocks situation in all of that is that inflation crashes decrease in some unspecified time in the future and the Fed is ready to ease charges again as a mushy touchdown happens. However that doesn’t look very probably any time quickly as mortgage charges are capturing again as much as 7% and the Fed reaffirms their aggressive price outlook. My baseline outlook for this 12 months is 3% PCE inflation at year-end. However even in that situation, which is comparatively optimistic, the Fed will stay at or close to 5% charges all 12 months. In different phrases, mortgage charges aren’t coming down any time quickly until one thing breaks and the Fed backpedals.

Struggle the Fed or Struggle the Market?

The beginning of 2023 raised an fascinating query. Because the inventory market rallies, dwelling costs stay agency and even homebuilders rallied, it’s important to ask your self whether or not you battle the Fed and stay bullish or battle the market and stay bearish about potential outcomes?

I’ve been saying this for over a 12 months now, however housing downturns are very lengthy drawn out occasions. There shall be many moments the place it appears to be like like there’s gentle on the finish of the tunnel. However I don’t suppose we’re there but. Housing is an enormous sluggish transferring beast and the fundamental math on affordability nonetheless appears to be like very dreary to me. I’ve a sense we’re going to be speaking about this housing downturn nicely into 2024 and hopefully by then issues have normalized sufficient that we are able to get again to life as ordinary. Till then, I nonetheless suppose it’s prudent to be cautious about how we navigate the present setting.

[ad_2]