[ad_1]

People’ retirement outlook doesn’t change all that a lot: one customary measurement persistently reveals that roughly half of working-age households might not be capable of afford their present way of life after retiring.

However do they even perceive what situation their retirement funds are in? This can be a essential query as a result of perceptions can have an effect on how a lot individuals will save for the long run.

The excellent news is that about 60 % of working-age {couples} and single persons are getting it proper, the Heart for Retirement Analysis finds. In different phrases, they predict, precisely, that they’re in hassle or that they’re in fairly good condition.

However that leaves important numbers who’re both over- or underestimating how a lot cash they might want to retire.

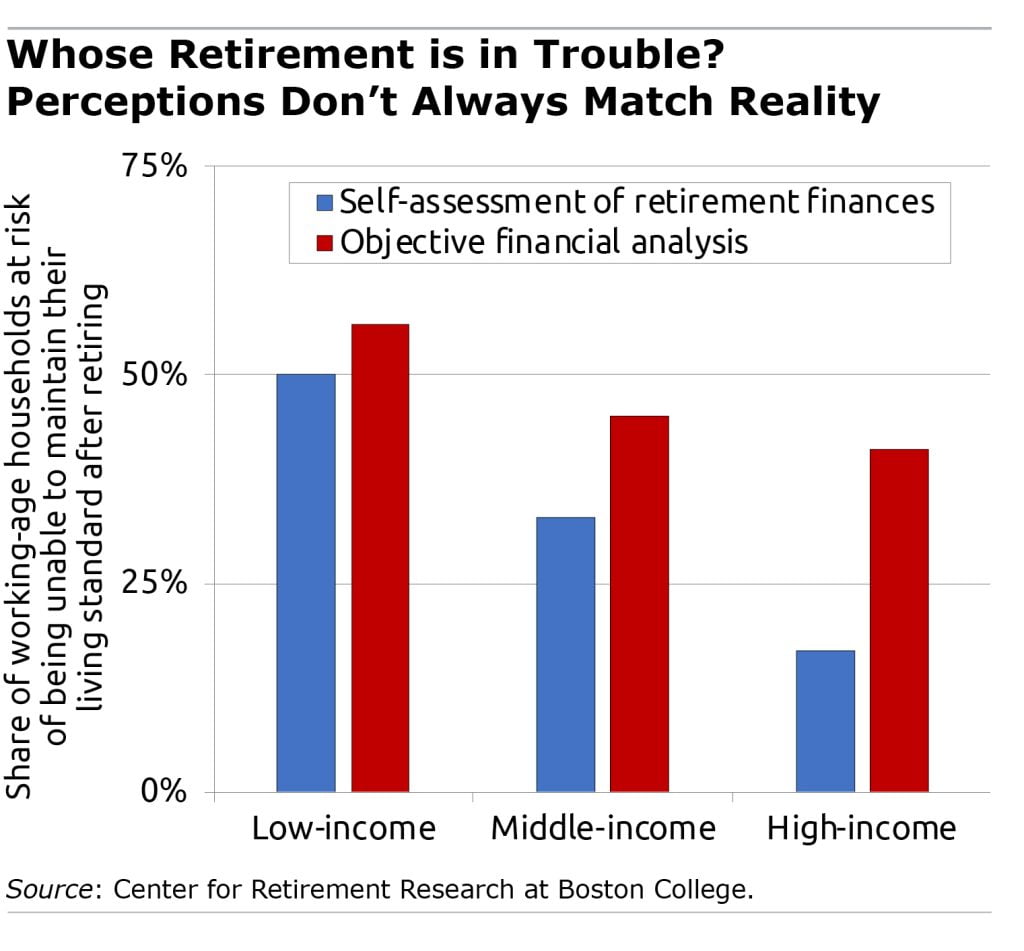

On this examine, the researchers used the Federal Reserve’s Survey of Shopper Funds in 2019 to gauge the accuracy of employees’ perceptions, utilizing their solutions to a query about how they really feel about their retirement funds. They’d 5 selections, starting from “completely insufficient” to “very passable.”

Their impressions have been paired up with an goal monetary evaluation, derived from the identical survey, of the proportion of U.S. households that aren’t saving sufficient to keep up their present lifestyle in retirement.

The 40 % who don’t have a superb deal with on their funds have been cut up into two teams – “not fearful sufficient” and “too fearful.” About 25 % are within the not-worried-enough camp and arguably worst off as a result of they don’t acknowledge the difficulty they’re in.

Employees at each earnings degree make this error, however high-income households do that greater than others. One purpose for his or her over-optimism is almost definitely that they personal costly homes and will put an excessive amount of inventory within the robust latest rise in costs on their substantial actual property holdings.

Excessive-income {couples} additionally underestimate their retirement threat when each of them are working however just one partner is saving for retirement. They may want extra financial savings to keep up their comparatively excessive residing customary after they retire.

The remaining 15 % of households who misperceive their funds are too fearful. This generally is a downside for anybody, and maybe extra so low-income employees, in the event that they’re making pointless sacrifices as we speak as a result of they’re unaware of all of the assets they’ll have in retirement.

When just one partner is working, for instance, the couple might not know the non-working partner will even obtain a Social Safety verify primarily based on the employee’s earnings. House fairness is a matter for low-income employees too. It’s a disproportionately giant share of their wealth, however they in all probability don’t have plans to faucet into it after they retire.

Planning for retirement is a sophisticated and difficult job however about 60 % of households have a superb intestine sense of their monetary scenario. The larger problem is the one in 4 that aren’t fearful sufficient. They should get a greater deal with on what retirement will appear like. They’ll’t provide you with a plan until they do.

Squared Away author Kim Blanton invitations you to observe us on Twitter @SquaredAwayBC. To remain present on our weblog, please be a part of our free electronic mail checklist. You’ll obtain only one electronic mail every week – with hyperlinks to the 2 new posts for that week – while you join right here. This weblog is supported by the Heart for Retirement Analysis at Boston Faculty.

[ad_2]