[ad_1]

After taking a short breather final week, the Indian equities prolonged their up transfer this time. After buying and selling buoyant and with restricted downsides all by way of the final 5 periods, the headline index ended on a decently constructive word. The Nifty oscillated in a 329.70 factors vary and whereas it ended in direction of its excessive level, the volatility gauge INDIAVIX as soon as once more declined in direction of its decrease ranges seen within the latest previous. The uncertainty across the US Debt Ceiling remained because the US markets awaited some deal however stayed largely buoyant. Amid sturdy setup, the benchmark index closed close to its essential ranges whereas posting an honest weekly achieve of 295.95 factors (+1.63%).

We enter a “decisive” week; going by the technical setup on the charts, markets could take a look at initiating a particular directional bias this week and no matter pattern it catches on could keep on at the very least for the brief time period. There’s additionally one thing essential that one wants to grasp concerning the US Debt Ceiling disaster. The debt ceiling is the utmost sum of money that the US can borrow cumulatively by issuing bonds. The debt ceiling was created beneath the Second Liberty Bond Act of 1917 and is often known as the debt restrict or statutory debt restrict. If U.S. authorities nationwide debt ranges bump up towards the ceiling, then the Treasury Division should resort to different extraordinary measures to pay authorities obligations and expenditures till the ceiling is raised once more which has been raised or suspended quite a few occasions through the years to keep away from the worst-case state of affairs: a default by the U.S. authorities on its debt.

A call on that is nonetheless awaited because the leaders negotiate to carry the debt but in addition curb spending within the course of. The negotiators are seen narrowing in on a two-year spending deal that might elevate the debt ceiling for a similar period of time, extending it previous the 2024 elections. Additionally it is essential to notice that the deadline for that is June 01, the deal is anticipated to come back in on the eleventh hour the Home of Representatives has left for a Memorial Day weekend; Monday is a vacation within the US.

Coming again to the markets, the Indices are on the cusp of a breakout and so they have closed at very decisive ranges. US Markets too have an identical setup; both the markets will stage a breakout over the approaching week or any retracement will put a intermediate prime in place someday. Both means, there are heightened prospects of a directional transfer getting began within the markets as the important thing indices are poised to maneuver out of their consolidation zone. Markets might even see a constructive begin to the week, the degrees of 18590 and 18700 are more likely to act as resistance; helps will are available at 18300 and 18150 ranges.

The weekly RSI stands at 61.35; it has marked a 14-period excessive which is bullish. It stays impartial and doesn’t present any divergence towards the worth. The weekly MACD is bullish and stays above its sign line.

The sample evaluation of the weekly chart exhibits that the NIFTY has closed under the most important double-top resistance at 18604; that is the most important excessive because the index was unable to surpass this and stage a breakout. In December 2022, NIFTY had retraced after a failed breakout tried forming an intermediate excessive of 18887.

Over the approaching days, two issues must be keenly watched. First would be the means of NIFTY to maneuver previous 18600 ranges; if this occurs, it’s set to check its lifetime excessive of 18887. Though the choices information exhibits the Index making an attempt to open up some room for itself on the upside, any incapability or failure to maneuver previous 18600 will usher in corrective declines for NIFTY. To sum up, there are heightened prospects of resumption of a directional transfer because the Index sits close to decisive ranges.

All in all, it’s strongly advisable that even though the markets are on the cusp of a decisive transfer, the transfer has not but occurred and it has the potential to go in both course. One should not go overboard in increase extreme directional positions till a transparent pattern emerges. Whereas persevering with to remain selective in approaching markets, a cautiously constructive outlook is suggested for the approaching week.

Sector Evaluation for the approaching week

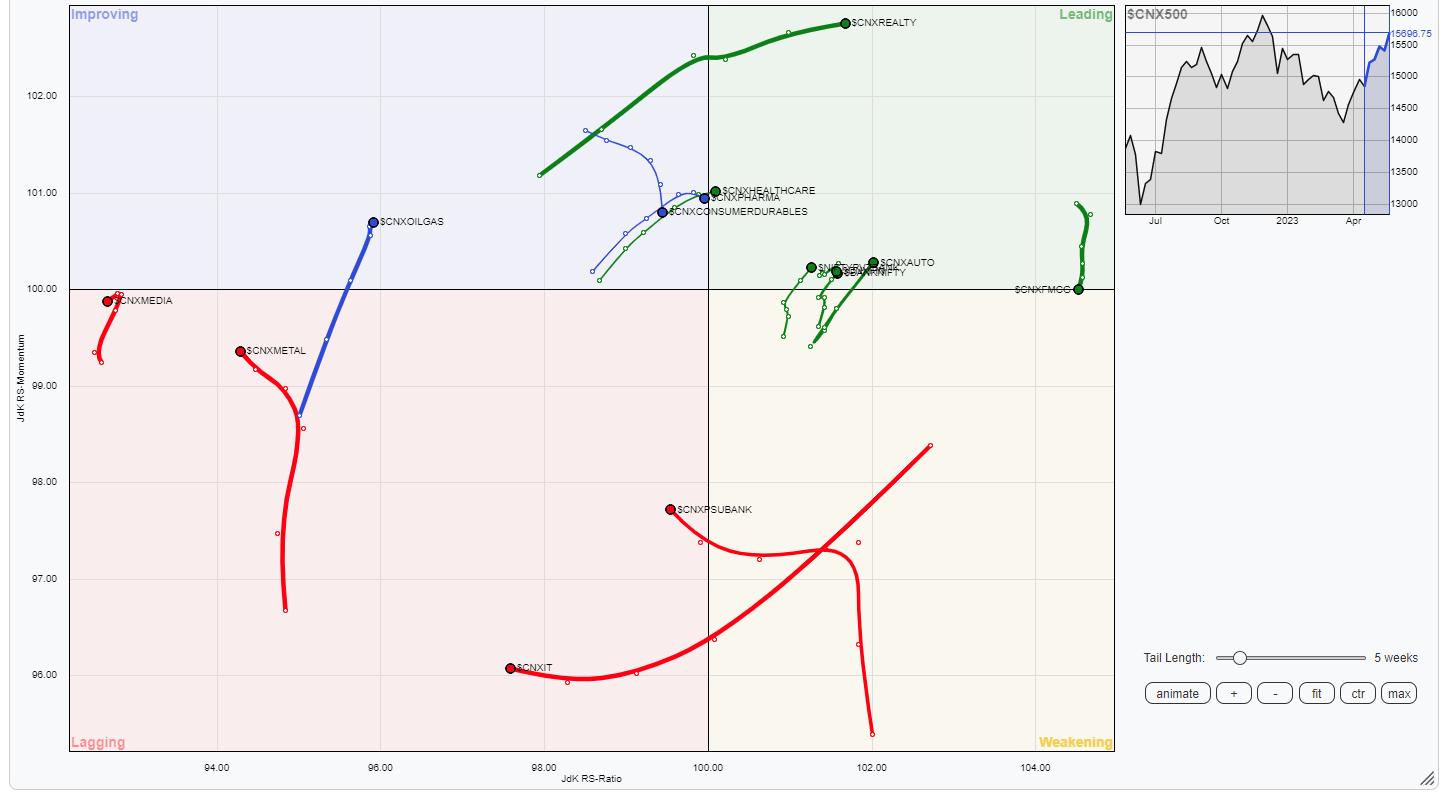

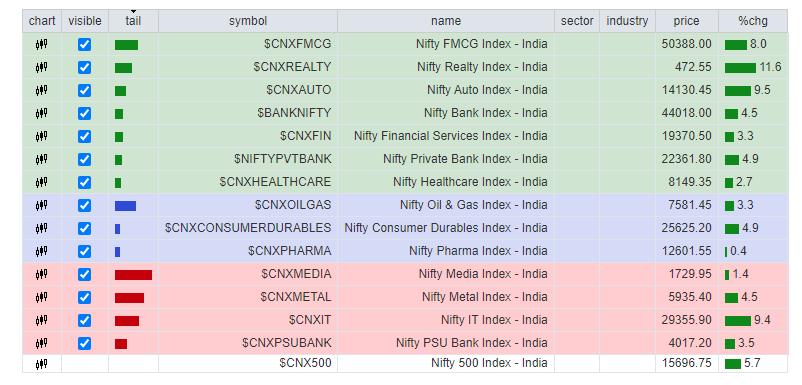

In our take a look at Relative Rotation Graphs®, we in contrast numerous sectors towards CNX500 (NIFTY 500 Index), which represents over 95% of the free float market cap of all of the shares listed.

The evaluation of Relative Rotation Graphs (RRG) exhibits that NIFTY Consumption, Midcap 100, Auto, Monetary Companies, and Realty are contained in the main quadrant. Nifty financial institution has additionally rolled contained in the main quadrant and we will count on these teams to comparatively outperform the broader NIFTY 500 Index. The FMCG index can be contained in the main quadrant however given the fast lack of relative momentum, it’s about to roll contained in the weakening quadrant.

The Nifty PSE and Infrastructure index are contained in the weakening quadrant.

The IT index continues to languish contained in the lagging quadrant together with the Steel and Media index. The opposite teams which are contained in the lagging quadrant are the Companies sector, Commodities, and the PSU Banks.

The NIFTY Pharma and the Vitality indices are seen firmly positioned contained in the bettering quadrant.

Vital Notice: RRG™ charts present the relative power and momentum of a gaggle of shares. Within the above Chart, they present relative efficiency towards NIFTY500 Index (Broader Markets) and shouldn’t be used straight as purchase or promote alerts.

Milan Vaishnav, CMT, MSTA

Consulting Technical Analyst

Milan Vaishnav, CMT, MSTA is a capital market skilled with expertise spanning near 20 years. His space of experience consists of consulting in Portfolio/Funds Administration and Advisory Companies. Milan is the founding father of ChartWizard FZE (UAE) and Gemstone Fairness Analysis & Advisory Companies. As a Consulting Technical Analysis Analyst and along with his expertise within the Indian Capital Markets of over 15 years, he has been delivering premium India-focused Impartial Technical Analysis to the Purchasers. He presently contributes every day to ET Markets and The Financial Occasions of India. He additionally authors one of many India’s most correct “Day by day / Weekly Market Outlook” — A Day by day / Weekly Publication, presently in its 18th 12 months of publication.

Subscribe to Analyzing India to be notified each time a brand new submit is added to this weblog!

[ad_2]