[ad_1]

You may have sufficient to retire if you’re snug together with your scenario, professional says

Critiques and suggestions are unbiased and merchandise are independently chosen. Postmedia might earn an affiliate fee from purchases made by way of hyperlinks on this web page.

Article content material

By Julie Cazzin with Allan Norman

Commercial 2

Article content material

Q: My spouse Caroline is 61 years outdated, retired from her job in southern Ontario final yr, and is now doing a bit part-time work. I’m 63 and deliberate to retire from my consulting job on the finish of this yr, however I’m unsure I can afford to, given the prolonged downturn within the inventory markets. My registered retirement financial savings plan (RRSP) has $210,000 and my tax-free financial savings account (TFSA) has $61,000. I even have $180,000 in my company, however it will improve to $250,000 by year-end. My spouse has $200,000 in RRSPs and $50,000 in a TFSA in addition to an listed pension of $55,000 per yr. Our house is price about $1 million and our retirement earnings purpose is about $90,000 per yr after tax. Can I nonetheless retire on the finish of this yr? — Simon and Caroline

Article content material

Article content material

Commercial 3

Article content material

FP Solutions: It appears there are a few points right here that require some considering by way of: Do you find the money for to retire? And what’s one of the best ways to optimize your retirement earnings?

I hear your concern that retiring now might now not be reasonable with the markets being down. As you already know, markets are going to maneuver up and down all through your retirement. Maybe it is a signal that even in case you mathematically find the money for, you don’t have sufficient to give you the reassurance to attract on that cash. Let’s work out the mathematics a part of the equation and see if that helps.

Simon, you will have three completely different accounts from which you’ll draw an earnings or a mix of incomes: a RRSP, TFSA and your funding firm (Investco), and so they all have completely different tax traits.

Commercial 4

Article content material

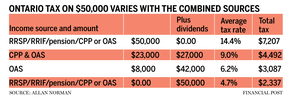

Within the accompanying desk, I’ve proven the common tax fee and whole tax paid based mostly on $50,000 earnings from differing sources.

Trying on the desk, you possibly can see the tax differential between non-eligible dividends and your different varieties of earnings. The query is, make the most of the tax variations? What in case you delay Canada Pension Plan (CPP) and Outdated Age Safety (OAS) to age 70 and draw $50,000 in dividends till you deplete the Investco investments and shut it up?

I don’t see an apparent cause for delaying withdrawals out of your Investco. The prices of investing inside a company are an annual tax return and accounting charges. Plus, the taxable parts of curiosity, dividends and capital positive factors are taxed at about 50 per cent, though there’s a refund mechanism that returns a few of the tax when a dividend is paid out.

Commercial 5

Article content material

Deferring your OAS and CPP to age 70 means rising them by 36 per cent and about 42 per cent, respectively. Mixed, that’s about $33,000 in right this moment’s {dollars} and $40,000 in precise {dollars} in comparison with a CPP plus OAS fee of $29,000 in precise {dollars} in case you began them at age 65. Delaying CPP and OAS till age 70 is price about an additional $11,000 per yr listed for all times.

I do know some individuals are involved that in the event that they die early, they might not gather as a lot CPP or OAS and that’s true. Nonetheless, remember, on this case, you might be saving $5,000 per yr in tax, and you might be winding down your Investco as soon as the investments are gone, saving you $1 to $2,000 in annual accounting charges.

The opposite cause chances are you’ll not like my suggestion of delaying your CPP and OAS is the concern of spending cash. It’s good to have some assured earnings and I’ve purchasers who inform me they don’t wish to draw a lot from their investments till their CPP and OAS begins. In your case, Caroline has an excellent base earnings for each of you, so this shouldn’t be a priority.

Commercial 6

Article content material

Now, what is going to mess up the suggestion of utilizing dividends first and delaying CPP and OAS is Caroline’s pension earnings. It’s doubtless that she is going to break up a few of her pension earnings with you, providing you with some taxable earnings. Nevertheless it doesn’t matter since there may be nonetheless a bonus in drawing down out of your Investco first.

-

Ought to we use TFSA financial savings to repay our mortgage?

-

What are the subsequent steps after paying off scholar debt?

-

How ought to a brand new widow finest arrange funds and investments?

After modelling this with prudent assumptions, I discovered that you’ll have no bother retiring on the finish of this yr, and might spend $90,000 per yr after tax, to age 100, after which go away an property with an after-tax worth of about $4 million. When you resolve to start out CPP and OAS at age 65, which means leaving an property worth of $3.8 million as a substitute. It’s whenever you and Caroline flip ages 83 and 81, respectively, when your internet price is bigger by taking CPP and OAS at age 70 relatively than 65.

Commercial 7

Article content material

Simon, you will have sufficient to retire if you’re snug together with your scenario. There are numerous methods to assemble retirement earnings and one of the best plan right this moment might not be one of the best plan when circumstances change. Don’t get too hung up on looking for probably the most optimum plan, however relatively give attention to one which works and that you’re snug with.

Allan Norman gives fee-only licensed monetary planning providers by way of Atlantis Monetary Inc. and gives funding advisory providers by way of Aligned Capital Companions Inc., which is regulated by the Funding Business Regulatory Group of Canada. Allan could be reached at alnorman@atlantisfinancial.ca

_____________________________________________________________

When you like this story, join the FP Investor Publication.

_____________________________________________________________

[ad_2]

Feedback

Postmedia is dedicated to sustaining a vigorous however civil discussion board for dialogue and encourage all readers to share their views on our articles. Feedback might take as much as an hour for moderation earlier than showing on the location. We ask you to maintain your feedback related and respectful. We now have enabled e mail notifications—you’ll now obtain an e mail in case you obtain a reply to your remark, there may be an replace to a remark thread you comply with or if a person you comply with feedback. Go to our Neighborhood Tips for extra data and particulars on modify your e mail settings.

Be part of the Dialog