MBW Explains is a brand new sequence of analytical options by which we discover the context behind main music trade speaking factors – and counsel what may occur subsequent…

WHAT’S HAPPENED?

On March 2, Common Music Group – the world’s largest music rights firm – introduced its full-year and This autumn monetary outcomes for 2022.

Inside these outcomes, as MBW lined right here, there have been an array of vital numbers for the music enterprise to chew on, not least the truth that UMG’s FY recorded music subscription streaming revenues grew, at fixed forex, by 10.0% YoY.

However wanting deeper into UMG’s outcomes, revealed for traders on this presentation, one different quantity actually stands proud.

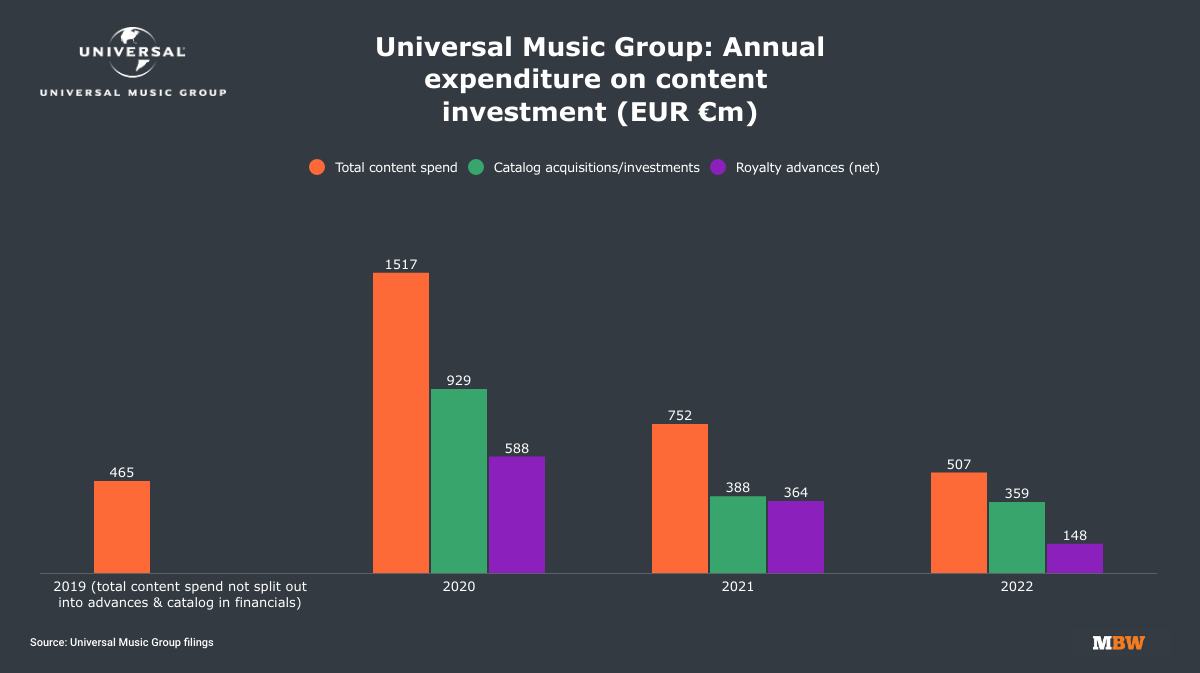

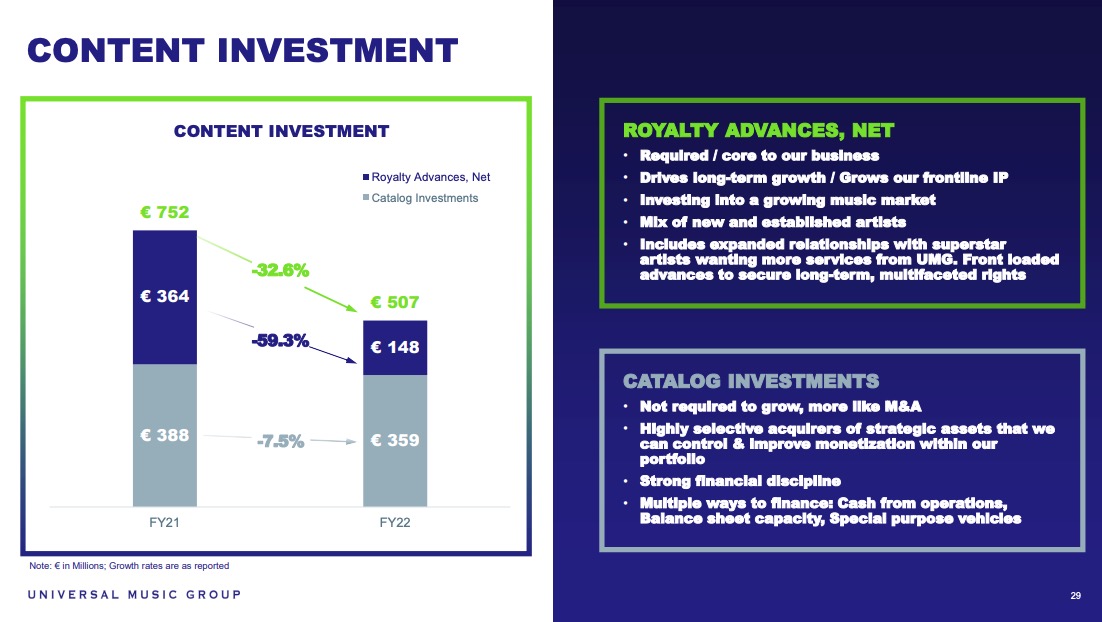

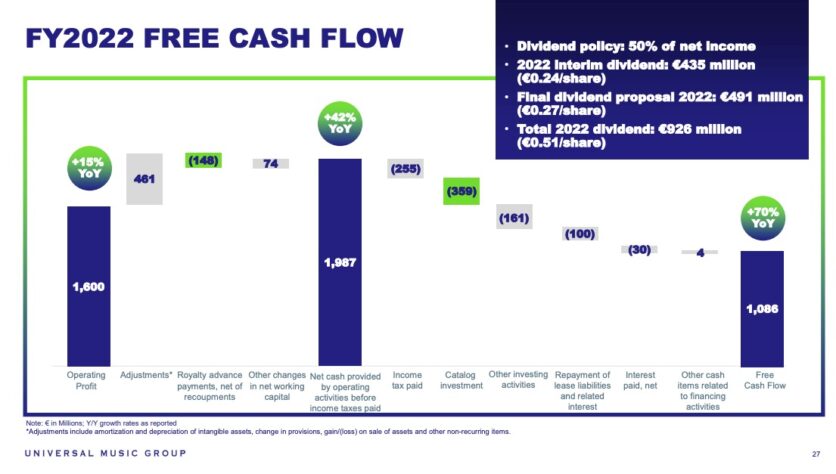

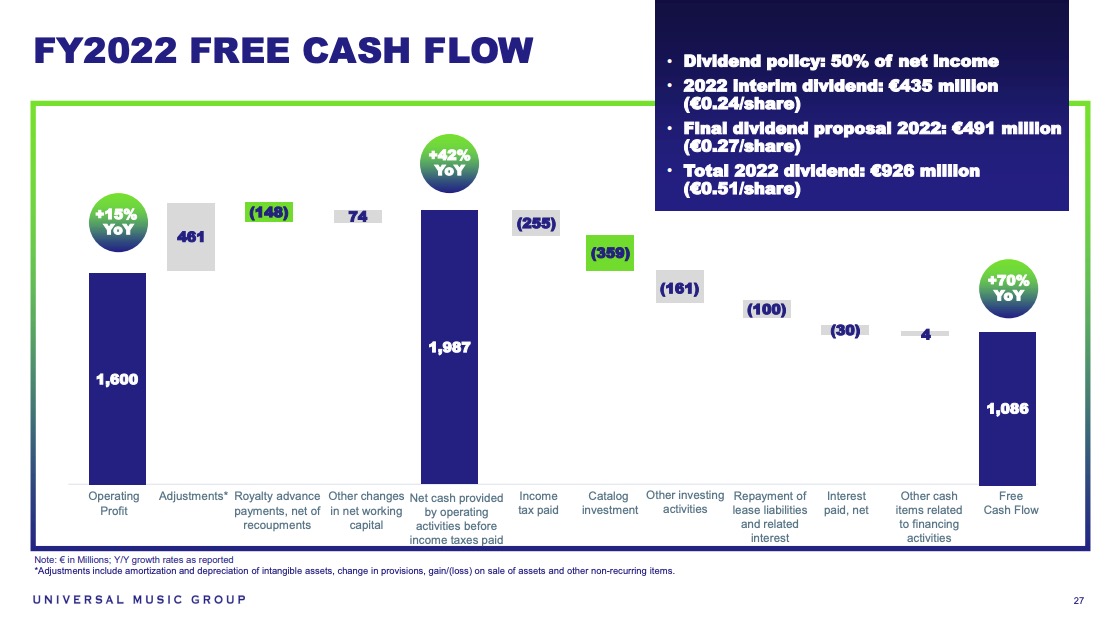

Within the calendar yr of 2022, in line with UMG’s administration, the agency spent a complete of EUR €507 million on ‘Content material Funding’.

That determine was made up of EUR €148 million in internet royalty advances (i.e. the gross sum of money superior to artists in 2022 much less complete recoupments), plus €359 million on what continues to be one of many music trade’s hottest speaking factors: Catalog acquisitions.

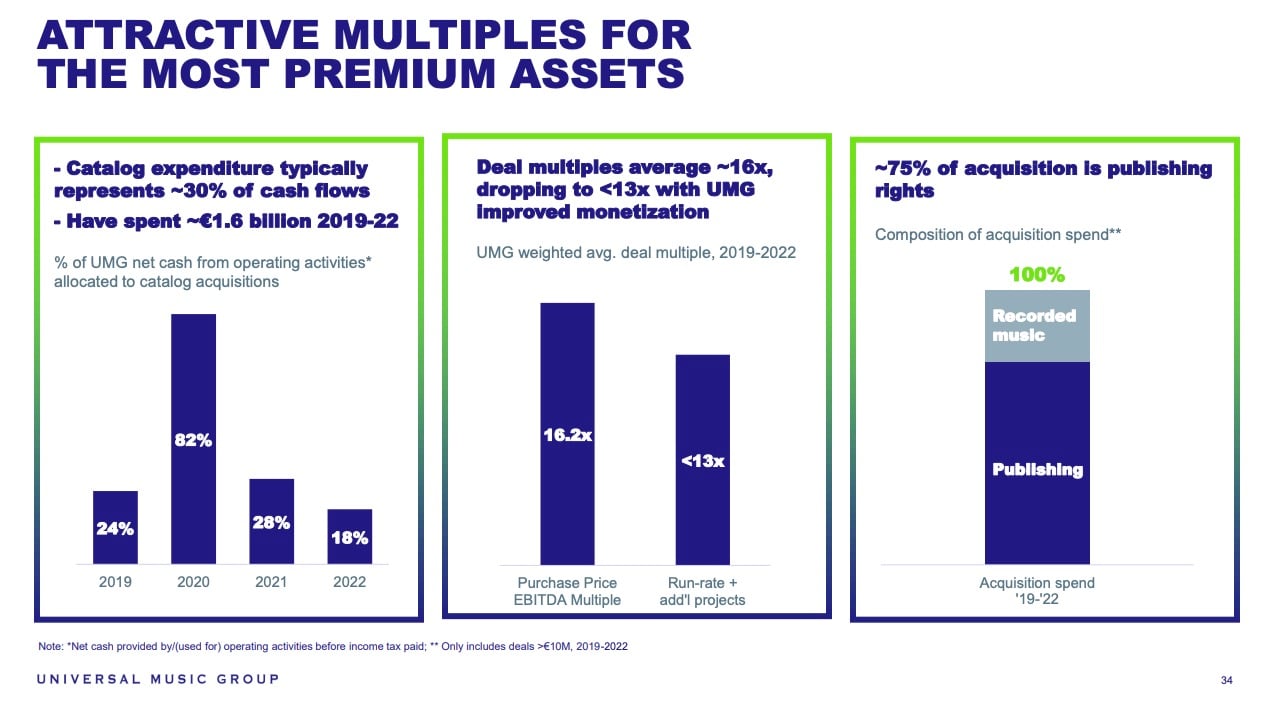

What was most exceptional about this set of numbers from Common, as illustrated within the chart beneath: how a lot UMG’s expenditure on catalog offers has fallen over the previous three years.

In 2020, for instance, the yr earlier than Common floated on the Amsterdam Euronext, UMG – then majority-owned by Vivendi – spent a whopping EUR €1.517 billion on ‘Content material Funding’… with over a billion US {dollars} (EUR €929 million) spent on catalog acquisitions.

Actually, from 2020 to 2022, Common Music Group’s annual expenditure on catalog rights shrunk by round two-thirds (-61%).

This slide from UMG’s newest annual monetary outcomes presentation highlights a 7.5% YoY slide in catalog spending in 2022

WHAT’S THE BACKGROUND?

One anomalous issue it’s a must to keep in mind right here: In 2020, Common made the largest acquisition in its historical past, spending someplace between USD $300 million and USD $400 million on the Bob Dylan publishing catalog.

Nonetheless, even with out that deal, UMG spent comfortably over half a billion {dollars} on catalog rights in 2020, way over it spent final yr (EUR €359m).

It’s additionally attention-grabbing to see that in 2021 – extensively seen because the frothiest yr on report for music M&A, with over USD $5 billion altering palms throughout the trade – UMG went in a special course than the broader market.

Common’s spending on catalog in 2021 considerably slowed, all the way down to lower than half what it spent within the prior yr (€388m vs €929m).

Does this deceleration in catalog spending (and the additional deceleration we’ve seen since) have a partial connection to UMG’s flotation in Amsterdam, which happened in September 2021, and was introduced in February 2021?

Maybe.

Spending giant sums of money on catalog acquisitions clearly negatively impacts Common’s Free Money Movement (FCF), which is a supply for annual dividends the corporate pays its shareholders.

Since floating in Amsterdam, UMG has introduced a coverage of paying its shareholders not less than 50% of its internet revenue annually in dividends.

In keeping with that coverage, in 2022, Common was proud to pay its shareholders the whopping sum of EUR €926 million in dividends, which labored out to greater than half of the corporate’s adjusted internet revenue (€1.454bn) within the yr.

That €926 million dividend outlay was nearly thrice the dimensions of the amount of money UMG spent on catalog acquisitions in the identical 12 months (€359m).

There may be, then, a possible little bit of push-and-pull between UMG’s goal to return piles of money to its shareholders, and its requirement to stay aggressive within the catalog M&An area. Successfully, spending massive cash on music rights will enhance UMG’s money circulate within the longer-term, however inevitably scale back it within the near-term.

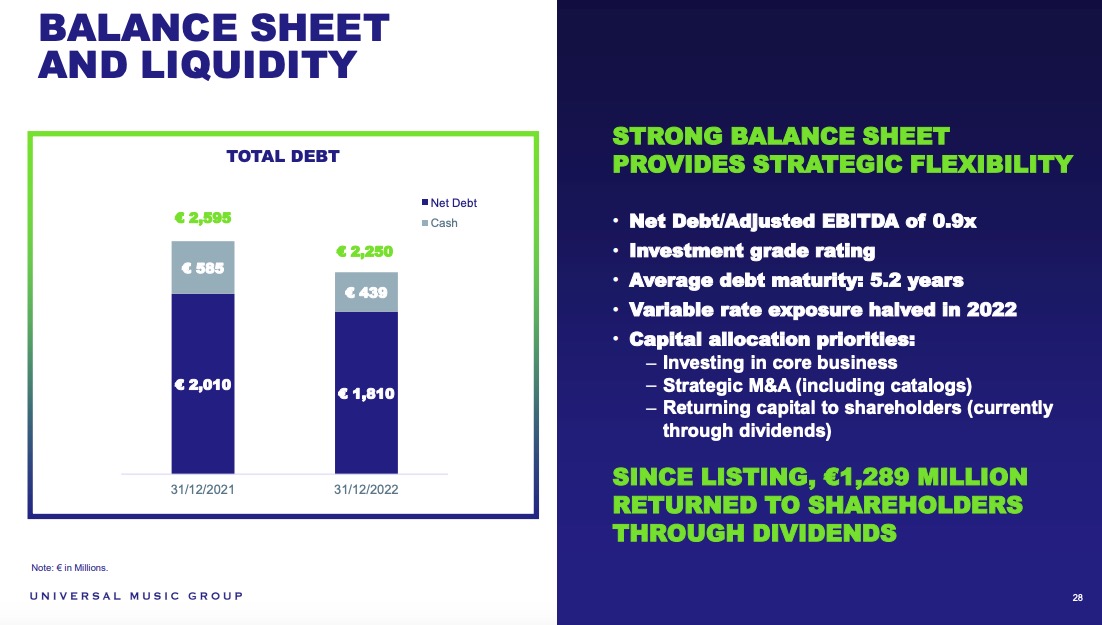

You’ll be able to see this fiscal yin-and-yang within the following two slides from UMG’s 2022 investor presentation beneath.

The primary slide highlights the unfavorable influence that its catalog acquisitions had on UMG’s money circulate in 2022 (whereas noting the €926m dividend paid out to traders that very same yr).

The second reveals the significance of UMG’s money pile (plus its debt pile) in its goal to “return capital to shareholders… through dividends”.

WHAT HAPPENS NOW?

In line with Common’s administration, monetary issues aren’t the first purpose for UMG’s evident prudency over catalog rights spending. It’s extra strategic than that.

Talking to traders on UMG’s This autumn earnings name final week, Common’s Chairman and CEO, Sir Lucian Grainge, characterised his firm’s reticence to spend billions on catalog rights annually as a significant optimistic for traders.

Grainge argued that many lively consumers in at present’s music’s M&A rights market are merely “passive individuals” within the revenue streams from music – i.e. they don’t have management of the licensing utilization of a given piece of music.

“UMG, then again, will not be within the passive rights enterprise,” mentioned Grainge. “We’re extraordinarily selective in rights acquisitions. Given our place within the trade, we see, I suppose, nearly every little thing. We go on most of it.”

UMG clearly likes this notion: though it may purchase a lot of the music catalog portfolios on sale out there proper now, it chooses to not.

“We’re extraordinarily selective in rights acquisitions… Given our place within the trade, we see, I suppose, nearly every little thing. We go on most of it.”

Sir Lucian Grainge, Common Music Group

Added Grainge: “We’ve got an excellent core enterprise with an abundance of high-return inside funding alternatives. A possible acquisition should due to this fact meet a really excessive threshold to ensure that us to determine to speculate.”

He continued: “As we now have an growing breadth of alternatives to contemplate, we proceed to make use of our money extensively focusing solely on the best alternatives out there to profitably speed up our progress.”

Common’s CFO, Boyd Muir, echoed Grainge’s sentiments over UMG’s heedfulness RE: the downsides of a rampant catalog acquisition technique.

Muir made the purpose that UMG’s “music rights acquisitions [account] for less than about 10% of our EBITDA progress during the last three years”.

With regards to Free Money Movement, Muir famous that Common’s FCF grew 17% YoYin 2022 “largely because of the expansion in adjusted EBITDA in addition to decrease spend on internet advances and catalog acquisitions“.

That being mentioned, Muir additionally made clear that Common’s catalog spending previously few years shouldn’t be characterised as minor.

“In complete, we now have spent €1.6 billion to amass rights since 2019,” he mentioned. “This has represented wherever between 18% and 82% of our annual internet money from operations.”

Muir additionally highlighted – as lined within the beneath slide – that within the catalog offers Common Music Group has accomplished previously three years (2019-2022), it has paid a median a number of of 16.2X every catalog’s prior-year EBITDA.

Nonetheless, he added: “After we account for a number of the fast worth we convey to catalog, together with some unlocked-up aspect, we see the typical a number of [becomes] lower than 13x our buy value.”

A FINAL THOUGHT…

It’s solely been a few weeks since MBW was mentioning that, after a sleepy H2 2022 interval, nine-figure catalog acquisitions had began sweeping again into the music trade in Q1 2023.

A kind of acquisitions was the $200 million buyout of Justin Bieber’s music publishing rights (and the artist’s recorded music revenue stream) by Blackstone-backed Hipgnosis Songs Capital (through Hipgnosis Tune Administration).

The Bieber track catalog has lengthy been administered by UMPG, so we could be 100% positive that Sir Lucian Grainge’s declare that his firm “sees nearly every little thing” in music utilized right here.

Ergo: UMG probably declined to match Hipgnosis’ spending stage on the deal. (Value noting: UMG owns Justin Bieber’s recorded music catalog.)

One other current instance of UMG bowing out of high-profile catalog acquisition alternatives: Scooter Braun, as CEO of HYBE America, simply spent ≈$300 million on hip-hop specialists High quality Management, as introduced final month – a deal which included rights to the QC’s label catalog.

QC’s music was beforehand launched through a three way partnership with UMG, that means that Grainge and his workforce, as soon as once more, would have undoubtedly had full sight of the High quality Management deal alternative. However identical to with the Bieber/Hipgnosis deal, Common once more declined to match the bid of a rival (this time, Scooter Braun).

Since MBW wrote that piece about massive cash washing again into music M&A in February, some extra main information has arrived: Larry Jackson’s gamma has acquired a catalog from Snoop Dogg that spans a variety of the rap legend’s personal hits, plus a wealth of different recordings on the Loss of life Row label.

Jackson has funded that acquisition (value unknown) utilizing cash from Eldridge – an organization based by billionaire Todd Boehly – which has beforehand acquired or co-acquired catalogs from the likes of The Killers (a Common-distributed recording act) and Bruce Springsteen (alongside Sony Music Group).

These are all examples of – as Lucian Grainge places it – UMG’s “extremely selective and opportunistic” catalog buyout technique.

However they’re additionally all examples of different firms choosing up helpful rights, as Common says: “No thanks.”

Not that you need to go away this text pondering that UMG doesn’t spend massive on catalog when it feels it must.

Don’t neglect that earlier this yr, information emerged that Common had acquired a run of belongings associated to Dr. Dre’s hits.

This acquisition got here with a reported $200 million+ price-tag – however that $200 million+ in spending was shared between UMG and Shamrock, which might have lessened Common’s monetary publicity within the deal.

We additionally shouldn’t neglect that UMG has made some very hefty outright acquisitions of its personal previously 12-24 months.

These embrace legendary catalogs from the likes of Neil Diamond and Sting, plus – in line with UMG’s newest investor presentation – the complete acquisition of the Money Cash recorded music portfolio, which has racked up over 12 billion streams thus far and contains a number of Drake albums.

In its presentation to This autumn presentation to traders, UMG neatly defined that its catalog acquisition technique in 2023 has 4 key pillars. Every of them (see beneath) is telling in regards to the firm’s hesitancy to overspend on shopping for too many rights.

Talking to traders this month, UMG’s Boyd Muir defined: “[We] run superior analytics to grasp the probably distribution of outcomes for [available] belongings. And from that, solely the very best belongings are chosen for acquisitions.”

Enjoying down the final word monetary significance of catalog acquisitions in UMG’s numbers, Sir Lucian Grainge added: “In the event you take a look at the totality of the incremental EBITDA coming in [to Universal] from buying catalogs, it’s actually not that vital in context of the totality of [our] enterprise.”Music Enterprise Worldwide

{kind=link}