[ad_1]

Usually, the large month-to-month Employment State of affairs Report is launched on the primary Friday of each month, which might imply March 3. However, due to a sophisticated system for the way such info is launched by the Bureau of Labor Statistics, and since February is a brief calendar month, this time the discharge is just not till March 10. So all of us get an additional week to ponder what the numbers are going to do.

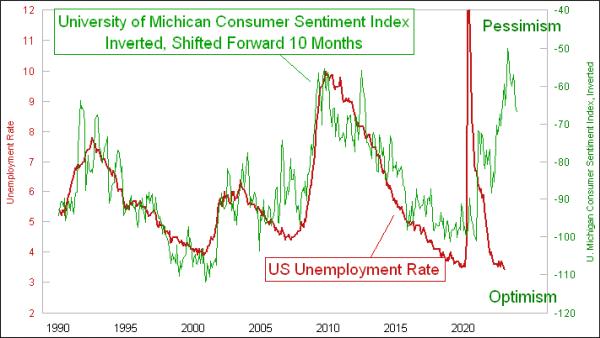

I’m anticipating that the latest months’ good numbers for unemployment are going to vary very quickly (in financial phrases). There are three nice main indications that assist us know what the lagging information of unemployment are going to do, and this week’s lead chart is the primary one. It reveals that modifications in client confidence precede modifications within the unemployment fee by about 10 months. This could imply an increase within the unemployment fee over the subsequent few months, to match the drop in client confidence that began greater than a yr in the past. The unemployment fee is at the moment somewhat bit late in making that upturn, which probably implies that it will must work further laborious to make up for misplaced time when the flip in the end comes.

An analogous message comes within the subsequent chart from a longer-term main indication. Modifications within the inflation fee result in corresponding modifications within the unemployment fee about 2 years later.

This revelation makes it all of the extra infuriating that, simply over 2 years in the past, numerous Federal Reserve officers have been bemoaning the inflation fee being too low, under their made-up goal of two%. They really wished to get inflation up, oblivious to the truth that this might imply an increase within the unemployment fee, which hurts their “twin mandate.” Sadly, they bought their want.

This mannequin requires a dramatic rise within the unemployment fee, resulting in a peak due in late 2024.

There’s yet one more intermarket relationship that’s attention-grabbing, and revelatory on this subject. It includes the inventory market, and a special approach of taking a look at employment.

The Employment-Inhabitants Ratio counts up each human alive within the U.S. (when you can consider the calculations) and compares that to how many individuals are working. It elements in not simply unemployed individuals, but additionally infants, college students, retirees, incarcerated, and so on. It clearly fluctuates up and down with the financial system, but additionally with altering demographics.

These altering demographics are usually not as attention-grabbing to ponder because the financial fluctuations, though demographics clearly do matter within the massive image. COVID threw these information for a loop, sending some individuals into an early retirement. Regardless that the official Unemployment Fee (U-3) is at an historic low at 3.4%, we nonetheless haven’t recovered to pre-COVID ranges when it comes to the Employment-Inhabitants Ratio.

The fascinating level addressed on this chart is that the actions within the Employment-Inhabitants Ratio are inclined to lag the actions of the inventory market by a few yr. This level is particularly legitimate with regards to inventory market declines, which are inclined to result in corresponding declines within the Employment-Inhabitants Ratio. Most attention-grabbing is how the bottoms within the inventory market are inclined to get echoed about 12 months later, on common, within the Employment-Inhabitants Ratio.

So if the October 2022 inventory market low actually is the underside for that bear market (a degree nonetheless but unproven), then we are able to reliably anticipate a backside within the Employment-Inhabitants Ratio that may be due in October 2023. That could be a little bit laborious to ponder, since we’ve not even seen a graduation of a decline in that ratio. And if the 2022 bear market really is just not over but, then that pushes again the tip level for the approaching decline within the jobs market, which the Fed appears so wanting to engineer, pondering that it’ll by some means assist inflation.

As an epilogue, it’s price noting in any dialogue concerning the precise employment or unemployment numbers that the Bureau of Labor Statistics (BLS) is having a tougher time gathering and tabulating these information. The employment and nonfarm payrolls numbers come from what is called the “institution survey”, which includes asking companies how many individuals they make use of. The unemployment fee numbers come from the “family survey”, which includes calling individuals on the telephone to ask how many individuals there are in a home, and what number of of them are working, on the lookout for work, and so on.

The BLS notes at https://www.bls.gov/osmr/response-rates/ that response charges for each of those surveys have been falling. Here’s a BLS chart displaying these response charges for numerous parts of the institution survey:

The BLS article linked above has explanations for all the acronyms listed within the chart, when you want to discover these variations additional. And here’s a chart displaying the falling response charges for the family survey.

The drop in family response charges is smart, as extra persons are migrating away from having landline telephones, and because the proliferation of telemarketers results in fewer individuals being keen to simply accept an incoming telephone name from a quantity that they don’t acknowledge. Political polling corporations are affected by these similar issues. These decrease response charges will understandably have an effect on the numerical accuracy of the info, and so it falls to us to not essentially consider the exact numbers that get revealed. However we are able to nonetheless consider typically within the story that they inform about modifications of development route that come from fluctuations in financial exercise.

Subscribe to High Advisors Nook to be notified at any time when a brand new publish is added to this weblog!

[ad_2]