[ad_1]

Part 80C of the Earnings Tax Act of 1961 is without doubt one of the hottest tax saving choices that enables for deductions as much as Rs 1.5 lakh every year. PPF contributions, five-year time period deposits and ELSS schemes are among the many listing of tax-free devices below this part. Nonetheless, there are numerous different tax-saving choices accessible that taxpayers could avail profit from. Listed here are a couple of:

1. Part 80E: Exemption of curiosity on schooling mortgage

Underneath part 80E, earnings spent to satisfy the curiosity element of schooling loans will not be taxable. There isn’t a restrict on the deduction quantity. Nonetheless, it must be famous that such a waiver is on the market for a most of 8 years or until the curiosity is paid. Any earnings spent past this time length is taxable. It may be utilized to satisfy the upper schooling prices of both self, kids or partner.

These tax deductions could be availed by people solely. Hindu Undivided Households (HUF) and corporations cannot avail of those tax exemptions.

2. Part 80TTA -Curiosity earnings generated from financial savings account deposits

Underneath part 80TTA, a deduction of as much as Rs 10,000 per 12 months on financial savings account curiosity is allowed. Nonetheless, if one maintains a number of financial savings accounts in numerous banks, whole cumulative curiosity is taken into account and is taxed below ‘earnings from different sources’.

If curiosity earnings exceeds Rs 10,000 in a 12 months, relying upon combination annual earnings, the surplus quantity over the cap is taxed at charges. This tax deduction could be availed by people and HUF. Apart from, NRIs might also avail of deduction below Part 80TTA.

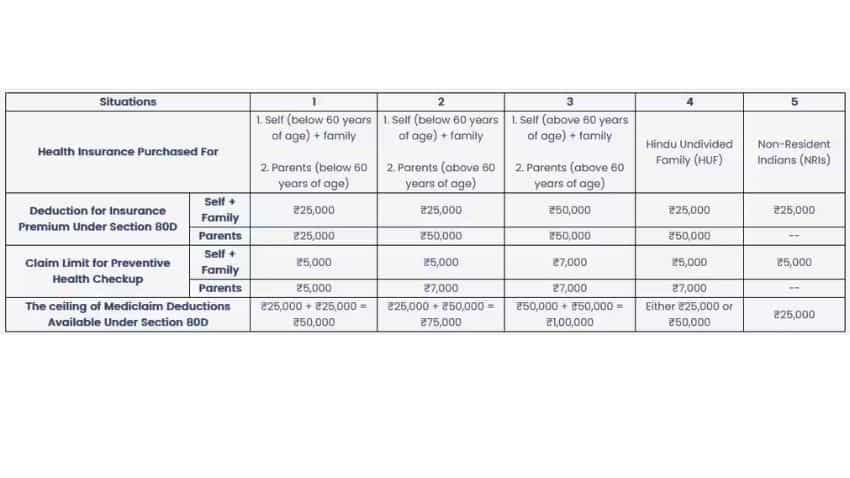

3. Part 80D- Deduction for Medical & Well being Insurance coverage

Underneath part 80D, cash spent on medical and medical insurance could be claimed. One is allowed to say a tax deduction of as much as Rs 25,000 on medical insurance coverage premiums per monetary 12 months. The deduction restrict of Rs 50,000 is allowed within the case of senior residents. The restrict applies to the premium paid in the direction of medical insurance bought for self, partner, kids

and fogeys.

Medical expenditure incurred on senior residents (aged 60 years or above) well being will not be coated below any medical insurance scheme.

4. Part 80G–Donations made to charitable organizations

One can declare a deduction below part 80G for any earnings donated to charitable organisations. Nonetheless, all donations don’t cowl below the part. Money donations are exempt from tax calculations for as much as Rs 2,000. Any money donation exceeding the identical doesn’t qualify for the deduction.

Such contributions need to be made to registered charitable organisations. NRIs are additionally eligible to say the advantages below Part 80G, provided that their donations are to eligible trusts or establishments.

5. Part 10(10D)- Life insurance coverage coverage payout

Underneath Part 10(10D), the complete sum assured disbursed upon maturity of life insurance coverage (maturity or dying profit) could be claimed for a tax rebate. Nonetheless, such dying profit is exempted from tax calculations whether it is availed after 1st April 2012, and whole worth premium prices are lower than the total sum assured. If the coverage is availed earlier than 1st April 2012, then the premium bills needs to be lower than 20% of the entire sum assured to be eligible for waivers below part 10(10D).*

HUFs, salaried and non-salaried people, international firms, physique of individuals and others are eligible for these tax exemptions.

[ad_2]